Accounting cycle- a bird eye view b

•Descargar como PPTX, PDF•

8 recomendaciones•1,288 vistas

A glimpse on background of accounting and accounting cycle by mounika ramachandruni

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Similar a Accounting cycle- a bird eye view b

Similar a Accounting cycle- a bird eye view b (20)

Más de mounika ramachandruni

Más de mounika ramachandruni (13)

Último

Último (20)

Accounting cycle- a bird eye view b

- 1. ACCOUNTING CYCLE By Mounika Ramachandruni

- 2. Introduction Accounting is the systematic and comprehensive recording of financial transactions pertaining to a business, and it also refers to the process of summarizing, analyzing and reporting these transactions to oversight agencies and tax collection entities. Accounting is one of the key functions for almost any business; it may be handled by a bookkeeper and accountant at small firms or by sizable finance departments with dozens of employees at large companies.

- 3. Background At one stage Luca Pacioli – the father of Accountancy brought a revolutionary change in the field of accountancy by writing a book on Mathematics- “Summa de Arithmetica Geometria Proportioniet Proportionlita” – containing a chapter – “De Computes it Scriptures”- in which Double Entry System of book keeping was explained. The Double Entry System is a recognized and generally accepted system all over the world and till date this system is being used widely with its basic principles unchanged.

- 4. Definition According to the American Institute of Certified Public Accountants [AICPA]; “Accounting is the art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events, which are, in part at least, of a financial character and interpreting the result thereof.”

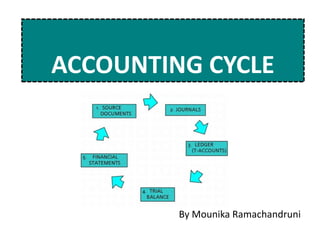

- 7. Accounting cycle The accounting cycle is the name given to the collective process of recording and processing the accounting events of a company. The series of steps begin when a transaction occurs and end with its inclusion in the financial statements. Additional accounting records used during the accounting cycle include the general ledger and trial balance.

- 8. Accounting cycle Upon the posting of adjusting entries, a company prepares an adjusted trail balance followed by the financial statements. An entity closes temporary accounts -- revenues and expenses -- at the end of the period using closing entries. These closing entries transfer net income into retained earnings. Finally, a company prepares the post-closing trial balance to ensure debits and credits match.

- 10. Journal An accounting journal entry is the method used to enter an accounting transaction into the accounting records of a business. The accounting records are aggregated into the general ledger, or the journal entries may be recorded in a variety of sub-ledgers, which are later rolled up into the general ledger.

- 11. Ledger In bookkeeping and accounting, a ledger is a book (or record) for collecting chronological transaction data from a journal, and organizing entries by account. The ledger provides the transaction history and current balance in each accounting system account, throughout the accounting period. At the end of the period, ledgers therefore serve as the authoritative source of data for building a firm's financial accounting reports.

- 12. Trail Balance Trial balance may be defined as an informal accounting schedule or statement that lists the ledger account balances at a point in time compares the total of debit balance with the total of credit balance. The trial balance is not an absolute or solid proof of the accuracy of books of accounts. Thus if trial balance agrees, there may be errors or may not be errors. But if it does not agree, certainly there are errors

- 13. Adjustment Entries Adjusting entries are journal entries recorded at the end of an accounting period to alter the ending balances in various general ledger accounts. This generally involves the matching of revenues to expenses under the matching principle, and so impacts reported revenue and expense levels.

- 14. Trading Account Trading account is prepared mainly to know the profitability of the goods bought (or manufactured) sold by the businessman. The difference between selling price and cost of goods sold is the,5earning of the businessman. Thus in order to calculate the gross earning,it is necessary to know: (a) cost of goods sold. (b) sales.

- 15. Profit or loss account The profit and loss account is opened by recording the gross profit (on credit side) or gross loss (debit side). For earning net profit a businessman has to incur many more expenses in addition to the direct expenses. Those expenses are deducted from profit (or added to gross loss), the resultant figure will be net profit or net loss. The expenses which are recorded in profit and loss account are ailed 'indirect expenses'.

- 16. Final accounts • Final accounts give an idea about the profitability and financial position of a business to its management, owners, and other interested parties. All business transactions are first recorded in a journal. • They are then transferred to a ledger and balanced. These final tallies are prepared for a specific period.