Indian IT Industry Up Skilling Trends

•

1 recomendación•655 vistas

Exploration of up-skilling trends (most popular themes for middle / senior management teams) in Indian IT Industyr: Contextualized by SWOT analysis and examination of Industry megatrends

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (18)

Destacado

Destacado (20)

Similar a Indian IT Industry Up Skilling Trends

Similar a Indian IT Industry Up Skilling Trends (20)

Indian IT Industry Up Skilling Trends

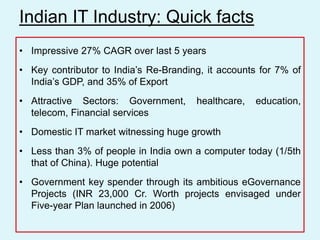

- 1. Indian IT Industry: Quick facts • Impressive 27% CAGR over last 5 years • Key contributor to India’s Re-Branding, it accounts for 7% of India’s GDP, and 35% of Export • Attractive Sectors: Government, healthcare, education, telecom, Financial services • Domestic IT market witnessing huge growth • Less than 3% of people in India own a computer today (1/5th that of China). Huge potential • Government key spender through its ambitious eGovernance Projects (INR 23,000 Cr. Worth projects envisaged under Five-year Plan launched in 2006)

- 2. Indian IT Industry SWOT STRENGTH: WEAKNESS: * Skilled manpower availability / * Known as low-cost destination Elaborate training infrastructure * High Attrition, Rising salary * Mature GDM, Quality Processes levels and other cost bases * Cash-rich; Can invest in * Linear business model and innovative business models concomitant scale-diseconomy OPPORTUNITIES: THREATS: * Exploding domestic market * Economic uncertainty / * High government spending and Currency fluctuations export-promotion Sops * Other emerging competitors * Biz-Model innovation for SMBs * Protectionist sentiments

- 3. IT Industry Landscape Global IT Industry Size: US$ 1614 Bn Indian IT Industry Revenue: US$ 71.7 Bn (Growing at CAGR 27%) *2009 Data

- 4. IT Products Industry Market Size (2007) Market Size (2011E) CAGR US$ 250 Bn US$ 339 Bn 7.9% Trends: – Stiff competition, Rapid technology changes – Changing customer needs forcing frequent product introductions – Cloud computing to gain momentum – Security issues becoming increasingly important Concern: – Growth rate expected to be subdued going forward – Customer-centric Innovation – Piracy major concern (Global loss ~US$ 48 Bn)

- 5. IT Services Industry Market Size (2008) Market Size (2012E) CAGR US$ 360 Bn US$ 441 Bn 2.8% Services lines: – Projects based – Outsourcing – Support / Training Trends: – Outsourcing to grow, but enhanced pressure on billing rates and Top line growth – Big players to try moving towards • Higher value-add services • Greater workforce utilization, and • Lowering SG&A expenses

- 6. IT Hardware Industry Market Size (2008) Market Size (2012E) CAGR US$ 594 Bn US$ 683 Bn 3.6% Growth rate in Asia is three times the growth rate in North America Trends: – Cost optimization across value-chain (Design, Manufacturing, Warranty, Operations etc) – Increased focus on R&D – Supply chain optimization required for reducing inventory

- 7. Domestic Market Growth 1.0 (2003 – 2008) • Off-shoring Revolution • Unprecedented growth of Indian Economy as well as in Domestic ICT demand; Revenue growth of 300% • Domestic demand mainly led by large Corporate / Public sector Growth 2.0 (2010 Onwards) • Growth to be led by End-users, SMBs • ‘Consolidation’ and ‘Leveraging’ of IT and telecom infrastructure built in Growth Phase 1.0, to realize greater business efficiencies and launch innovative product/solution offering • Increased adoption and acceptance of ‘game changing’ technologies • Governments’ economic stimulus is unlocking market potential

- 8. Industry Megatrends • Strategic M&As / Alliances for Platform creation • Alliance-driven Sales model • Greater Partnership with client for End-to-end offering – Larger share of wallet and connecting with stakeholders so as to create barrier to entry • Sharper customer segmentation, Sub-Verticalization and Domain-Specific Branding • Multiplicity of Business Models and Growth Agendas • Cost optimization across Value-Chain

- 9. Era of Strategic Alliances

- 10. Outsourcing Relationship - Roadmap Source: Harvard case-study

- 11. IT / ITeS Industry: Challenges • Growth: Organic / Inorganic, linear vs. non-linear • Coping with speed of change and continually innovate / reinvent itself • Develop innovation capability. Also ability to sell Innovation • Successful differentiation (Branding)/ staying ahead on the curve (Business model Innovation) • Identifying strategic targets for Acquisition / Alliances. Quantifying Synergy • Alliance management. Moving up the value-chain with clients • Ability to sell high value-add services (e.g. Business Process Integration) • Transitioning top-talent from Technocrats to Business Managers • Sales team need to understand data and communicate Business Value of IT • Attrition

- 12. Strategic options to cope with these Challenges • Understand Competitive Strategy; Invest in Execution Capability • Industry is in Growth stage hence Identify Niches, Innovate in Business Model and invest in Branding • Scenario Planning: Understand forces shaping Business Landscape • Change Management - to successfully transition Organization • Appreciation of Marketing, and Customer-Centric Innovation • Co-opetition: Cooperate in Value-Chain, Compete in Core-competence • Develop capability of Cross-cultural Integration, Strategic Alliance Management and Strategic Account Management

- 13. Strategic options … • Move beyond Delivery Capability: Understand Client’s Business – Because your customer may not understand Technology • Create various platforms to bring together key Decision Makers and enable them to experiment with IT • Proactively build enhanced awareness to transformation potential of IT adoption • Evolve multi-tiered Capability Enhancement Strategy – Tackle knowledge-attrition of your Senior Managers – Create Leadership Pipeline; Support transition through Leadership stages • Strategic Human Resource Management – HR as Strategic Partner. Alignment with Business Strategy – Robust Supply Chain, Continuous re-skilling, Attrition Management

- 14. Up-skilling trends in IT Industry • Building innovation culture – Foster Innovation and Creativity, Revolutionize service offering – Successfully differentiate from overcrowding competition – Identify approaches to non-linear revenue growth – Building a learning organization (Knowledge-centric organization) • Planning under uncertainty – Appreciate the changing Business Dynamics – Discern inflection points. How current business models might be rendered obsolete – Establish organizational ability for adapting to possible futures • People management for higher performance – Energizing the workforce – Leading high-performance teams – Leading in a matrix organization – Influencing without authority – Managing the new generation talent - tools to motivate people

- 15. Up-skilling trends… (2) • Developing Strategic Thought Process – Strategic Planning Process – Strategy Execution – Competitive Strategy, Globalization Strategy, Corporate Strategy • Customer Centricity – From being operations/product focused to being customer focused and developing the sales and marketing competencies – Silo-busting that promotes Customer Focus • Leadership Development – Transitioning through Leadership Stages (Ram Charan’s Model) – Change management: Overcome overt and covert resistance to change – Self Leadership: Breaking the inward looking mould – Looking at the big picture, developing a vision and motivating people to achieve that vision

- 16. Up-skilling trends… (3) • Product companies – Customer centric innovation – Leveraging informal networks for Innovation • Corporate teams – Finance for Non-Finance Executives – Value creation through M&A – Post-merger integration • Sales and Marketing – Accelerating Sales Performance – Relationship management : Engaging the client like a strategic partner – Marketing Strategy, Services Marketing, B2B Marketing • HR Teams – Aligning HR with Business Strategy – Strategic Talent Management – Cross-cultural integration

- 17. THANKS Please share your comments: mrinalsri@gmail.com