1. Portfolio Construction and Risk Management

g

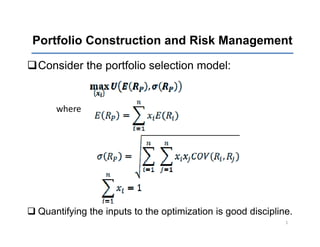

Consider the portfolio selection model:

where

Quantifying the inputs to the optimization is good discipline.

1

2. Portfolio Construction and Risk Management

g

Risk Management

Start with quantification of what you know (risk)

S f f ( )

Prepare for what is not knowable (uncertainty)

Challenge simplifying assumptions

C f

1) Only care about the mean and variance of the

probability di t ib ti of portfolio returns

b bilit distribution f tf li t

a) Ignore skewness (asymmetry) and kurtosis (fat tails)

b) Event risk

c) Market failure

d) Government Intervention

e) Investment horizon – liquidity demand versus

provision 2

3. Portfolio Construction and Risk Management

g

2) Parameter Stationarity (or one period model)

a) Regime Change

b) Time variation characteristics (bonds)

c) Cuspiness (securitized asset tranches)

d) Dynamic interaction (liquidity->fundamentals-

>liquidity => downward spiral

e) Time-varying covariance structure (i.e., correlations

Time varying

increase during crisis periods)

3

4. Portfolio Construction and Risk Management

g

Risk Management Approaches

1) Multi-Dimentional Risk Analysis (calculate sensitivity exposures

to state variables)

2) Stress tests on each exposure

3) Value-in-Stress (multiple scenario analysis)

4) Value at Risk (VaR) is probabalistic

a)

) Requires covariance matrix estimation

q

b) i.e., 95% VaR is L= –V x 1.645 x portfolio standard deviation .

There is a 5% chance of loosing more than L.

c) Distributional assumption for tail risk

d) Parameter estimation

i. Historical data (with or without forward looking adjustments)

ii. Forward simulation

e) Model the tail of the distribution

4

5. Portfolio Construction and Risk Management

g

Dealing with the unknowable

1) Stop Loss (then what?)

2) Flight to quality hedges

3) Long/short strategies (no net market or macro-factor

macro factor

exposures)

4) L k

Lock-ups

5) Portfolio Insurance

5

6. Portfolio Construction and Risk Management

g

General Valuation Equation

x1 x2 xN

V0 = + + ...+

(1+ R1 ) (1+ R1 )(1+ R2 ) (1+ R1 )...(1+ RN )

For bonds, the cash flows in the numerator are expected coupons

and principal payment(s) in each period.

For common stock, N is infinity and the numerator contains

stock

expected cash flows to equity holders.

The R' s are the per period expected required rates of return to

compensate investors for the riskiness of their respective cash

flows.

Risk Premi m is a function of priced risk factors and the sec rit ’s

Premium f nction security’s

sensitivity to those exposures.

6

9. Pension Plan Asset-Liability Management

2006 Pension Protection Act

Requires underfunded plans to move toward a 100% funding level

d f d d l d f d l l

Provisions come into effect on a rolling schedule over several years

9

10. Pension Plan Asset-Liability Management

Provisions combined with market performance trends are affecting asset

allocations now

10

11. Pension Plan Asset-Liability Management

Major Factors Affecting Pension Plan Funding Status

Performance of assets

Performance of assets

Company contributions

Number of employees covered and cost per employee

Discount rates used to calculate the present value of

Discount rates used to calculate the present value of

future obligations

AA rated Long‐dated corporate bonds

AA rated Long dated corporate bonds

Average of AAA, AA, and A rated corporate bonds

Note that the discount factors have fallen sharply during 2009 =>

Note that the discount factors have fallen sharply during 2009 =>

increase in PV of future obligations

11

12. Pension Plan Asset-Liability Management

Asset Allocation: Select a portfolio that minimizes the

standard deviation of the plan’s surplus

12

13. Pension Plan Asset-Liability Management

Liabilities rate of return series:

Rate of change in the present value of future liabilities for the

change in discount rates (AAA‐A corporate bond rates

g ( p

prescribed by the 2006 pension protection act).

The term structure of liabilities in this example is that of the

The term structure of liabilities in this example is that of the

average pension plan.

The riskiness of the plan’s liabilities in the time‐series of

Th i ki f h l ’ li bili i i h i i f

returns is defined by the time period selected.

13

14. Pension Plan Asset-Liability Management

Asset Allocation: Select a portfolio that minimizes the

standard deviation of the plan’s surplus

14