Peer Company Analysis

•Descargar como PPTX, PDF•

3 recomendaciones•4,259 vistas

INTERNSHIP PROJECT PRESENTATION ON PEER COMPANY ANALYSIS OF CORPORATES IN ANDHRA PRADESH

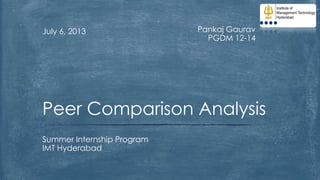

![Portfolio of companies

Company name

Amara Raja Batteries

Limited

Andhra Petrochemicals

Ltd

Divi's Laboratories Ltd

Credit Rating

Industry

CRISIL AA / CRISIL A1+

Auto Ancillaries

ICRA A-/ ICRA A2+

CARE AA+ /CARE A1+

Chemicals

Pharmaceuticals

Floriculture& Agri

business

Textile & Textile

Products

Cement product

Construction &

Infrastructure

Cement

Not rated yet

Neha International

Suryalata Spinning Mills

Ltd

ICRA]BB+/ICRA A4+

Visaka Industries Limited CARE A+/CARE A1+

CRISIL A- Negative/

CRISIL A2+

Ramky Infra

Anjani Portland Cement CARE BB/CARE A4](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (20)

Destacado

Destacado (20)

Similar a Peer Company Analysis

Similar a Peer Company Analysis (20)

Más de Pankaj Gaurav

Más de Pankaj Gaurav (9)

Último

Último (20)

Peer Company Analysis

- 1. July 6, 2013 Pankaj Gaurav PGDM 12-14 Peer Comparison Analysis Summer Internship Program IMT Hyderabad

- 2. Portfolio of companies Company name Amara Raja Batteries Limited Andhra Petrochemicals Ltd Divi's Laboratories Ltd Credit Rating Industry CRISIL AA / CRISIL A1+ Auto Ancillaries ICRA A-/ ICRA A2+ CARE AA+ /CARE A1+ Chemicals Pharmaceuticals Floriculture& Agri business Textile & Textile Products Cement product Construction & Infrastructure Cement Not rated yet Neha International Suryalata Spinning Mills Ltd ICRA]BB+/ICRA A4+ Visaka Industries Limited CARE A+/CARE A1+ CRISIL A- Negative/ CRISIL A2+ Ramky Infra Anjani Portland Cement CARE BB/CARE A4

- 3. Methodology A dossier per company is to be prepared. Capacity Utilisation Current Order Book Business Analysis Cost structure Board of Directors/ Management Team Shareholding Pattern Industry Analysis FIRM Financial Summary

- 4. How to analyze a company •Legal Status •Bankers •Management team •Shareholding Pattern •Lines of Business •Business Segments •Major Products / Services •Geographic presence Basic Information Fundamental Analysis •Analyze financial statement •Analyze financial metrics •Identify the trends in the business Business Overview Comparative Analysis • Price/Earnings Ratios • Earnings Expectations • Capacity utilisation • EBITDA margins • EBDITA interest coverage • Net debt/EBITDA

- 5. Key Metrics Definitions used for Peer Com. Market Capitalization: The total market value of all of a company's outstanding shares. Market capitalization is calculated by multiplying a company's shares outstanding by the current market price of one share. The investment community uses this figure to determine a company's size, as opposed to sales or total asset figures.. P/E (TTM) : A valuation ratio of a company's current share price compared to its per-share earnings. The timeframe of the past 12 months used for reporting financial figures. Calculated as : P/E=(Market Value per Share/ Earnings per Share (EPS) Enterprise Multiple: A ratio used to determine the value of a company. The enterprise multiple looks at a firm as a potential acquirer would, because it takes debt into account - an item which other multiples like the P/E ratio do not include. Enterprise multiple is calculated as: Enterprise Multiple= Enterprise value/EBITDA

- 6. Key Metrics Definitions(cont.)… Return On Equity - ROE: The amount of net income returned as a percentage of shareholders equity. Return on equity measures a corporation's profitability by revealing how much profit a company generates with the money shareholders have invested. Calculated as : ROE = Net Income/ Shareholder's Equity Debt/Equity Ratio: A measure of a company's financial leverage calculated by dividing its total liabilities by stockholders' equity. It indicates what proportion of equity and debt the company is using to finance its assets. Calculated as : D/E ratio = Total Liabilities/ Shareholder’s Equity Return on Capital Employed (ROCE): A ratio that indicates the efficiency and profitability of a company's capital investments. Calculated as: ROCE= (EBIT/Total Asset – Current Liability)

- 8. Anjani Portland Cement Anjani Cement is a small enterprise with Market cap of 308.9 Millions as compared to its Sagar Cement, Deccan Cements &NCL Industries. Note: All amounts are in Millions Particulars Manufacture of Cement FY09 FY10 FY11 FY12 FY13 Revenue 1520.976 1527.145 2096.67 3386.547 3260.958 0.41% 37.29% 61.52% -3.71% Revenue Growth Security Printing Product Segment Operating EBITDA 475.976 315.518 452.052 764.765 585.704 Operating EBITDA MARGIN 31.29% 20.66% 21.56% 22.58% 17.96% Interest cover 5.6 3.81 1.054 1.64 - Net profit Gas based power generation 267.925 215.505 15.411 234.111 428.414 Adjusted Debt/EBITDA 1.256 6.783 5.910 3.726 3.946 Debt/ Net worth 1.002 3.166 3.995 3.486 2.717

- 9. Anjani Portland Cement(cont.) 8 7 3000 Interest cover 6 2814.149 2641.246 2500 2311.428 5 Adjusted Debt/EBITDA 2125.05 2000 4 3 Net adjusted debt/EBITDA 1500 2 Debt/ Net worth 1000 1 Return on cap employed (EBIT/cap employed) 0 FY09 FY10 FY11 FY12 FY13 Total net worth Total DEBT 500 571.951 570.355 671.085 661.136 807.112 850.438 0 FY09 FY10 FY11 FY11 FY11

- 10. Peer Comparison: Cement Manufacturing Company Madras Cement Chettinad Cement India Cements KCP Sagar Cements Andhra Cements Deccan Cements NCL Inds. Anjani Portland Raasi Cement Bheema Cements Market Cap P/E (TTM) EV/EBIDTA ROE (Rs. in Cr.) (x) (x) (%) 5,069.40 12.89 8.21 2,710.48 19.7 4.68 1,724.82 9.77 6.66 358.99 10.35 4.76 327.71 37.32 3.92 184.04 0 17.01 133.77 18.3 2.74 89.1 0 3.07 29.42 9.52 4.26 22.29 0 0 19.94 0 23.87 ROCE D/E (%) (x) 18.3 14.6 18.7 17 8.2 10.5 18.1 17.3 18.4 20.5 5 6.5 24.3 19.2 25.5 21.4 22.3 20.31 0 0 0 0 1.22 0.99 0.72 0.99 0.93 1.61 1.45 1.6 3.38 0 1.17

- 11. Peer Comparison : Cement Manufacturing(cont.) 40 4 35 Madras Cement 30 Chettinad Cement 3.5 Madras Cement 3 Chettinad Cement India Cements 25 KCP 20 Sagar Cements Andhra Cements 15 Deccan Cements 10 NCL Inds. Anjani Portland 5 Raasi Cement 0 (x) (x) (%) (%) P/E (TTM) EV/EBIDTA ROE ROCE India Cements 2.5 KCP Sagar Cements 2 Andhra Cements Deccan Cements 1.5 NCL Inds. 1 Anjani Portland Raasi Cement 0.5 Bheema Cements Bheema Cements 0 D/E

- 12. Key Business Risks & Issues Deterioration in financial performance Stretched liquidity position Weak capital structure High exposure to group companies Moderate industry outlook Power & fuel Procurement

- 13. NEHA INTERNATIONAL LTD. A premium grower of cut roses, NEHA brings in 19 years of rich experience in the field of floriculture. Note: All amounts are in Millions Particulars Cut Flowers Machinery Trading Sales Product Segment FY10 FY11 FY12 Revenue 559.725 881.795 784.610 57.54% -11.02 Revenue Growth Operating EBITDA 169.936 234.974 115.696 Operating EBITDA MARGIN 30.36% 26.65% 14.75% Interest cover 4.89 7.5 2.88 Net profit 122.96 178.125 63.36 Adjusted Debt/EBITDA 1.01 0.898 2.507 Debt/ Net worth 0.298 0.125 0.129

- 14. Peer Comparison: Floriculture& Agri business Company Market Cap P/E (TTM) EV/EBIDTA ROE ROCE D/E (Rs. in Cr.) (x) (x) (%) (%) (x) JVL Agro Indus 168.57 2.79 0.74 20.1 20.7 Genera Agri 68.40 6.39 0 42 39.3 Neha Intl. 20.23 23 31.32 0.5 4.21 Pion. Agro Extr. 7.53 0 5.6 9.8 13.5 Elegant Floricul 8.56 142.67 34.26 0.1 0.3 Gemini Agritech 4.87 0 51.5 0 0 Naisargik Agri 3.97 325 0 0.4 0.5 German 3. Gardens 77 6.65 0 12.6 7.7 0.6 0.07 0.07 1.53 0.03 1.56 0 2.24

- 15. Peer Comparison : Floriculture& Agri business(cont.) 350 45 300 40 JVL Agro Indus 250 Genera Agri 200 (x) (x) P/E (TTM) EV/EBIDTA (%) Elegant Floricul 15 Gemini Agritech 0 Pion. Agro Extr. 20 Elegant Floricul 50 Neha Intl. 25 Pion. Agro Extr. 100 Genera Agri 30 Neha Intl. 150 JVL Agro Indus 35 Gemini Agritech 10 Naisargik Agri Naisargik Agri 5 German Gardens German Gardens 0 ROE ROCE 2.5 JVL Agro Indus 2 Genera Agri Neha Intl. 1.5 Pion. Agro Extr. 1 Elegant Floricul Gemini Agritech 0.5 Naisargik Agri 0 D/E German Gardens

- 16. Key Business Risks & Issues High import tariff vis-avis African countries Low availability of dedicated perishable carriers Inadequate cold chain management Availability of basic inputs, including quality seeds and planting materials Low level of product diversification and differentiation, vertical integration Lack of quality irrigation and skilled manpower

- 17. Divis Lab Divis Laboratories focused on developing new processes for the production of Active Pharma Ingredients (APIs) & Intermediates Note: All amounts are in Millions Generic API’s Particulars FY09 FY10 FY11 FY12 Revenue 12024.76 9759.46 13436.634 19200.806 -18.84% 37.68% 42.90% Intermediates Revenue Growth Peptide Building Blocks Operating EBITDA 5033.225 4395.916 5244.089 7493.317 Operating EBITDA MARGIN 41.86% 45.04% 39.03% 39.03% Interest cover 62.884 139.669 310.591 183.599 Net profit 4166.418 3403.365 4292.694 5332.641 Net Adjusted Debt/EBITDA 3.235 4.440 1.124 1.052 Debt/ Net worth 1.140 1.145 0.318 0.362 Product Segment

- 18. Divis Lab (cont.) 350 Total net worth Total DEBT 300 250 21311.965 19244.034 200 17961.725 16129.132 150 14143.551 100 13184.445 50 0 7720.191 5724.31 FY09 FY10 FY11 FY12 interest cover 62.88438492 139.6369001 310.5918892 183.5996206 Net adjusted debt/EBITDA 3.23586011 4.440459281 1.124815197 1.05200087 debt/ net worth 1.140387729 1.459601371 0.318694891 0.362246794 FY09 FY10 FY11 FY12

- 19. Peer Comparison: Pharmaceutical industry EV/EBIDT Company Market Cap P/E (TTM) A ROE (Rs. in Cr.) (x) (x) (%) Lupin 38,090.09 30.22 21.23 Divi's Lab. 12,796.44 20.93 13.41 Jubilant Life 1,970.54 25.04 21.18 Hikal 695.99 27.28 5.65 Elder Pharma 690.45 7.5 6.59 Shilpa Medicare 631.98 13.73 9.34 Vinati Organics 491.53 7.16 5.63 Dishman Pharma. 443.04 7.01 5.44 Shasun Pharma. 352.05 14.43 7.48 Orchid Chemicals 343.8 0 7.67 Marksans Pharma 333.28 8.4 0 Nectar Lifesci. 320.75 3.74 6.25 Suven Life Scie. 277.98 9.02 10.21 Sequent Scien. 273.82 0 7.62 Granules India 262.25 8.69 4.12 ROCE D/E (%) (x) 23.4 22.7 27.3 34.1 3.1 6.4 22.4 18.2 12.9 13 16.3 18 33.2 31.3 6.8 10.2 14 8.9 9.7 8.3 0 0 9.7 11.2 11.3 9.1 -3.9 5.9 11.7 15.2 0.3 0.02 1.43 1.53 1.25 0.19 0.75 0.8 1.05 1.75 0 1.22 0.64 1.58 0.57

- 20. Peer Comparison: Pharmaceutical Industry(cont.) 40 2 Lupin 35 Divi's Lab. 30 Jubilant Life Hikal 25 Elder Pharma 20 Shilpa Medicare Vinati Organics 15 Dishman Pharma. 10 Shasun Pharma. Divi's Lab. Jubilant Life 1.4 Hikal Elder Pharma 1.2 Shilpa Medicare Vinati Organics 1 Dishman Pharma. Shasun Pharma. 0.8 Orchid Chemicals 0.6 Marksans Pharma 0.4 Marksans Pharma Nectar Lifesci. Suven Life Scie. Nectar Lifesci. 0 -10 Lupin 1.6 Orchid Chemicals 5 -5 1.8 (x) (x) (%) (%) P/E (TTM) EV/EBIDTA ROE ROCE Suven Life Scie. Sequent Scien. Sequent Scien. 0.2 0 Granules India D/E

- 21. Key Business Risks & Issues Product concentration risk Moderate customer concentration Long working capital cycle Ability of the company to diversify the customers and products base Forex risk related to the exports Maintaining the profitability levels

- 22. Ramky Infrastructure Limited Ramky Infra principally operates in two business segments: construction (carried out by Ramky Infra itself) and developer business (implemented through SPVs). Note: All amounts are in Millions Particulars Construction business Developer business Others Product Segment FY10 FY11 FY12 FY13 Revenue 21102 32344.6 39708.7 37735.532 53.28% 22.77% --4.97% Revenue Growth Operating EBITDA 3110.79 -2493.99 -4169.372 5534.385 Operating EBITDA MARGIN 14.74% -7.71% -10.5% 14.67% Interest cover 2.760 -1.945 -1.929 1.6777 Net profit 1273.6 2061.3 2440.7 1512.51 Adjusted Debt/EBITDA 6.2744 -10.239 -8.85 7.515 Debt/ Net worth 1.82 1.221 1.697 1.671

- 23. Peer Comparison: Infrastructure & Construction & Real Estate Company Market Cap P/E (TTM) EV/EBIDTA ROE ROCE D/E (Rs. in Cr.) (x) (x) (%) (%) (x) DLF 31,796.13 63.35 16.41 6 8.2 JP Associates 11,627.82 23.19 9.94 9.6 9.4 Unitech 5,507.31 29.65 14.93 3.1 4.8 Prestige Estates 5,456.50 19.76 14.86 6.2 7.9 Godrej Propert. 4,107.79 33.49 31.59 5.9 7.2 Phoenix Mills 3,566.93 26.65 17.89 6.5 8.5 Jaypee Infratec. 3,513.99 5.06 8.15 24.5 13.8 Mahindra Life. 1,722.41 17.67 13.02 8.4 9.8 HDIL 1,608.96 2.83 7.08 3.9 7.2 Punj Lloyd 1,074.34 54.83 7.28 1.6 8.4 IVRCL Assets 735.98 0 50.79 -2 1.3 IL&FS Engg. 285.98 0 10.1 -28.1 2.3 Ramky Infra 274.27 4.58 5.86 15.5 18.2 Gammon India 264.13 0 5 4.5 11.6 1.3 2 0.43 0.52 0.88 0.1 1.28 0.25 0.4 1.06 0.27 2.22 0.88 1.25

- 24. Peer Comparison: Infrastructure & Construction & Real State(cont.) 80 DLF JP Associates 60 40 JP Associates 2 Unitech Prestige Estates Godrej Propert. Phoenix Mills Godrej Propert. 1.5 Phoenix Mills Jaypee Infratec. 20 Mahindra Life. HDIL Jaypee Infratec. Mahindra Life. 1 HDIL Punj Lloyd 0 (x) (x) (%) (%) P/E (TTM) EV/EBIDTA ROE ROCE IVRCL Assets Punj Lloyd 0.5 IVRCL Assets IL&FS Engg. IL&FS Engg. Ramky Infra Gammon India -40 DLF Unitech Prestige Estates -20 2.5 Ramky Infra 0 D/E Gammon India

- 25. Key Business Risks & Issues Deterioration in the Ramky Infra group’s financial risk profile, particularly its liquidity Higher reliance on short-term debt Stretch in working capital cycle Cost overrun in execution of its BOT projects

- 26. Amara Raja Batteries Limited Amara Raja Batteries Limited (ARBL), the largest manufacturer of Standby Valve Regulated Lead Acid (VRLA) batteries in India Note: All amounts are in Millions Particulars Revenue VRLA batteries FY09 FY10 13212.35246 FY11 FY12 FY13 17688.29 23809.298 29810.775 12.13% Revenue growth 14814.99016 19.39% 34.60% 25.20% 3560.489 4711.956 Operating EBITDA 1927.831427 2699.51243 2651.52 Four-wheeler batteries: Operating EBITDA MARGIN 0.145911293 0.182214932 0.149902563 0.149541956 0.158062177 Interest cover 8.676343026 33.52347354 73.06736429 76.26900714 Two-wheeler batteries Net profit 804.786707 1670.333868 1480.96 2150.626 2867.047 Adjusted Debt 3749.279934 1933.51446 2076.48 1341.65 1359.513 Net worth 4055.864344 5436.42719 6459.27 8234.69 10598.134 Adjusted Debt/EBITDA 1.944817312 0.716245807 0.783128168 0.376816218 0.288524129 Net adjusted debt/EBITDA 1.580235743 0.484843862 0.612969165 -0.266887498 -0.58327837 Debt/ Net worth 0.704833715 0.167737823 0.154748137 0.103872763 0.082394033 0.222 0.345 0.299 Product Segment Return on cap employed (EBIT/cap employed) 0.329 0.339

- 27. Peer Comparison: Auto Ancillaries Industry Company Bosch Motherson Sumi Exide Inds. Amara Raja Batt. WABCO India Amtek India Amtek Auto Bosch Chassis Federal-Mogul Go Wheels India Market Cap P/E (TTM) EV/EBIDTA ROE (Rs. in Cr.) (x) (x) (%) 27,192.56 30.83 16.58 12,304.75 26.2 13.29 10,336.00 19.77 12.66 4,708.96 16.08 6.38 3,109.53 23.78 12.28 1,874.85 13.99 9.28 1,506.15 5.62 7.47 1,238.98 45.81 0 1,129.29 0 17.24 829.77 26.03 5.47 ROCE D/E (%) (x) 18.6 23.9 27.8 24.4 16.3 23.1 29.3 32.9 33.5 45.9 8 9.5 6.7 7.6 7.2 9.8 -2.3 3.9 15 21.1 0.05 0.76 0 0.13 0 1.22 0.84 0.09 0.43 1.57

- 28. Peer Comparison: Auto Ancillaries Industry(cont.) 50 1.8 1.6 40 Bosch Motherson Sumi 30 Exide Inds. Amara Raja Batt. Bosch Motherson Sumi 1.2 Exide Inds. Amara Raja Batt. 1 WABCO India 20 Amtek India Amtek Auto 10 WABCO India 0.8 Amtek India Amtek Auto 0.6 Bosch Chassis Bosch Chassis Federal-Mogul Go Wheels India 0 (x) -10 1.4 (x) (%) Federal-Mogul Go 0.4 Wheels India 0.2 (%) 0 P/E (TTM) EV/EBIDTA ROE ROCE D/E

- 29. Key Business Risks & Issues Multi-tiered and highly fragmented domestic auto supplier segment Long working capital cycle Capex requirement for innovations in technology

- 30. Andhra Petrochemicals Ltd APL was established with a capacity to produce 30,000 MTPA of Oxo Alcohols at Visakhapatnam, Andhra Pradesh, India. Note: All amounts are in Millions Particulars Revenue FY10 FY11 FY13 4594.894 6056.059 5627.6 219.6% 31.8% 7.07% 165.381 515.6907 245.7531 1034.648 0.11504069 0.112231251 0.040579707 0.183852442 3.342473875 1.698188264 0.160681727 10.4339309 -53.805 356.352 300.147 31.187 Adjusted Debt Manufacture of OxoAlcohols 1567.291 1492.295 778.698 633.828 Net worth 1618.725 1876.321 2127.09 2158.277 Adjusted Debt/EBITDA 9.476850424 2.893779159 3.168619236 0.612602547 Net adjusted debt/EBITDA 8.872349303 1.785110726 3.048087695 0.484546435 Debt/ Net worth 0.886641647 0.777770968 0.29947581 0.293673148 Revenue growth % Operating EBITDA Operating EBITDA MARGIN Interest cover Net profit Product Segment 1437.587 FY12

- 31. Peer Comparison: Chemical Industry EV/EBIDT Company Market Cap P/E (TTM) A ROE (Rs. in Cr.) (x) (x) (%) Castrol India 16,169.64 36.05 20.39 Pidilite Inds. 13,783.81 30.21 19.58 Godrej Inds. 10,592.32 277.19 28.98 Guj Fluorochem 3,074.45 7.72 7.96 BASF India 2,367.75 19.65 11.06 Linde India 2,251.39 104.35 15.35 Gulf Oil Corpn. 784.77 15.74 7.7 Balaji Amines 108.54 3.49 3.71 Oriental Carbon 106.14 3.88 3.6 Sah Petroleum 104.28 0 3.75 Panama Petrochem 102.36 8.62 0.37 Andhra Petrochem 97.29 15.68 3.24 ROCE D/E (%) (x) 71.4 104.3 29.7 36.6 10 10.5 32.8 38.4 10 12.9 4.1 4 10.5 9.1 27.5 24.3 23 23.7 0.2 23.3 16.9 24.8 15 18.7 0 0.1 0.46 0.37 0.16 0.75 0.57 1.33 0.63 0 0.05 0.52

- 32. Peer Comparison: Chemical Industry (cont. ) 120 Castrol India 100 Pidilite Inds. 80 Godrej Inds. 60 Guj Fluorochem Linde India 20 Castrol India 250 Pidilite Inds. Godrej Inds. 200 Guj Fluorochem BASF India 150 BASF India 40 300 Linde India Gulf Oil Corpn. 100 Balaji Amines Gulf Oil Corpn. 0 (x) (%) (%) EV/EBIDTA ROE ROCE Balaji Amines Oriental Carbon Sah Petroleums 1.4 Oriental Carbon 50 Sah Petroleums Panama Petrochem 0 Andhra Petrochem P/E (TTM) Castrol India Pidilite Inds. 1.2 Godrej Inds. 1 Guj Fluorochem BASF India 0.8 Linde India 0.6 Gulf Oil Corpn. 0.4 Balaji Amines Oriental Carbon 0.2 Sah Petroleums 0 Panama Petrochem D/E Andhra Petrochem

- 33. Key Business Risks & Issues Weakening Profit due to intermittent high feedstock prices and weak global demand High power costs in the near term on account of lower availability of power from the grid Lack of integration benefits Import duty differentials and Rupee-US Dollar parity levels Threat of cheaper imports from regions / countries like the Middle East, South East Asia, South Africa and Russia High concentration risks due to dependence on a single feedstock supplier

- 34. Visaka Industries Limited Visaka Industries was established in 1981 to manufacture corrugated cement fiber sheets. Note: All amounts are in Millions Particulars Revenue FY09 FY10 FY12 FY13 7551.65 9181.59 46.49% 7.89% 14.24% 21.58% 1285.262 394.197 859.214 742.958 1092.218 0.219560286 0.06434850 0.12999170 0.09838353 0.118957392 Interest cover 6.574881043 1.92429538 7.11934459 3.99857425 5.972332147 359.38 572.11 450.74 343.41 506.878 1687.503 1620.349 1888.5 1462.77 2920.194 Adjusted Debt Product Segment 6609.76 Balance Sheet Debt (1) Synthetic Yarn 6125.97 Operating EBITDA MARGIN Building Products 5853.8 FY11 1696.021 1888.897 2159.571 1733.967 3215.892 Net worth 1877.945 2357.282 2613.512 2864.76 3260.466 1.319591647 4.79175894 2.51342622 2.33386947 2.944368249 1240.431 1280.177 1621.031 1195.167 2880.017 Net adjusted debt/EBITDA 0.965119174 3.24755642 1.88664407 1.60866024 2.636851801 Debt/ Net worth 0.898590214 0.68738021 0.72259090 0.51060821 0.895637004 Revenue growth Operating EBITDA Net profit Adjusted Debt/EBITDA Net adjusted debt

- 35. Peer Comparison: Cement Products Company Ramco Inds. Hil Ltd Everest Inds. Visaka Inds. Sahyadri Inds. Siporex India Vardhman Concr. Sanghvi Asbestos U.P.Asbestos Roofit Inds. Market CapP/E (TTM) EV/EBIDTA ROE (Rs. in Cr.) (x) (x) (%) 382.35 7.09 4.63 263.26 4.34 2.94 256.18 4.88 4.02 128.47 2.53 3.65 36.09 1.85 4.05 12.18 4.91 0 8.57 4.88 3.5 2.88 0 80 0.93 0.31 66.91 0 0 5.27 ROCE (%) D/E (x) 15.4 19.2 19.5 16.6 10.1 21.9 14.9 23 20.9 16.5 13.3 18.8 0.59 0.3 0.47 0.71 1.64 0.95 0 -1.7 8.7 33.6 0 3 11.5 21.4 0 0.46 1.86 1.92

- 36. Peer Comparison: Cement Product(cont.) 80 Ramco Inds. 70 60 Hil Ltd 50 Everest Inds. 40 Visaka Inds. 30 Sahyadri Inds. 20 Siporex India 10 Vardhman Concr. 0 Sanghvi Asbestos -10 (x) EV/EBIDTA (%) ROE (%) ROCE U.P.Asbestos 90 Sanghvi Asbestos 10 U.P.Asbestos 0 P/E (TTM) Siporex India Vardhman Concr. Sanghvi Asbestos U.P.Asbestos D/E Vardhman Concr. 20 Sahyadri Inds. 0 Siporex India 30 Visaka Inds. 0.5 Sahyadri Inds. 40 Everest Inds. 1 Visaka Inds. 50 Hil Ltd 1.5 Everest Inds. 60 Ramco Inds. 2 Hil Ltd 70 Roofit Inds. 2.5 Ramco Inds. 80 Roofit Inds. Roofit Inds.

- 37. Key Business Risks & Issues Assured long-term supply of raw materials at reasonable prices Possible impact of any adverse regulations/restrictions with respect to the use of asbestos

- 38. Suryalata Spinning Mills Ltd Suryalata Spinning Mills Limited is one of the largest producers of Yarn. Note: All amounts are in Millions Particulars Textilesspinning Synthetic/Blen ded Product Segment Total Income FY10 FY11 FY12 1731.7 2599.0 2538.8 57.2 197.9 42.3 Net profit Operating Profit Margin(%) 12.08 16.9 3.64 Return On Capital Employed(%) 13.72 27.66 10.77 Interest Cover 2.94 5.70 1.95 Debt Equity Ratio 5.55 2.83 1.94 54.58 36.27 Number of Days In 47.02 Working Capital

- 39. Peer Comparison: Textiles- spinning Market Company Cap P/E (TTM) EV/EBIDTA ROE (Rs. in Cr.) (x) (x) (%) RSWM Ltd 298.52 4.4 9.07 Sangam India 131.27 2.54 5.6 Winsome Textile 88.6 4.6 9.95 Banswara Syntex 56.05 4.65 5.72 Jindal Cotex Ltd 41.72 9.46 29.78 Deepak Spinners 18.03 1.39 2.94 Suryalata Spg. 17.98 1.62 5.34 Samrat Spinners 15 0 0 East Ind.Syntex 13.32 0 0 Rel. Chemotex 11.3 1.79 5.51 ROCE (%) -7.3 8.9 -9.6 8.9 -5.7 14.1 9.4 16.6 6.1 7.5 4.7 10.3 6.1 11.5 0.7 15.8 10 12.3 -14.3 14.3 D/E (x) 4.07 2.93 2.43 3.74 0.55 1.1 1.88 1.37 0 1.62

- 40. Peer Comparison: Textiles- spinning(cont.) 35 30 25 RSWM Ltd 20 Sangam India Winsome Textile 15 Banswara Syntex 10 Jindal Cotex Ltd 5 Deepak Spinners Suryalata Spg. 0 -5 (x) (x) (%) (%) (x) -10 P/E (TTM) EV/EBIDTA ROE ROCE D/E -15 -20 Samrat Spinners East Ind.Syntex Rel. Chemotex

- 41. Key Business Risks & Issues Subdued demand scenario Timely infusion of additional equity for the debt funded capex Rising interest rates Operating profitability impacted by political scenario

- 42. Limitations • Due to unwillingness to share annual reports by Pvt. Limited companies, company analysis can be made for public listed companies whose annual reports are available on its website. • No information on term loan repayment schedule is made available by firms, which makes a bit difficult to understand a firm’s credit profile. • For doing business analysis, capacity utilisation information is not available in annual reports/websites, due to which % utilisation and average realisation per unit can’t be determined.

- 43. Key Learnings • Understanding of the credit profile of a company based on its financial performance, cost structure, financial structure and investments made in past 5 years • Understanding of key credit rating issues form rationale based on past ratings given by other credit rating agencies in India • Understanding of the nature of industry in Andhra Pradesh and building a perspective on respective industry outlook • Identification of key risks exist in respective industry based on industry outlook • Understanding of the fundamentals of credit rating methodology with respect to corporate sector of India