Call US 📞 9892124323 ✅ Kurla Call Girls In Kurla ( Mumbai ) secure service

Italy's international competitiveness

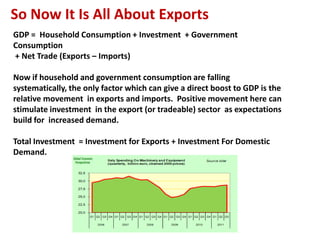

1. So Now It Is All About Exports

GDP = Household Consumption + Investment + Government

Consumption

+ Net Trade (Exports – Imports)

Now if household and government consumption are falling

systematically, the only factor which can give a direct boost to GDP is the

relative movement in exports and imports. Positive movement here can

stimulate investment in the export (or tradeable) sector as expectations

build for increased demand.

Total Investment = Investment for Exports + Investment For Domestic

Demand.

2. Just Not Sufficiently Competitive?

While Italian exports surged back

after the financial crisis recession

they never in fact attained their pre-

crisis level, and now they are once

more declining again. In addition,

even though Italy’s goods trade

deficit has reduced substantially over

the last 12 months, it is still a DEFICIT.

As we can see in the chart on the

right, the Italian economy was on an

unsustainable path from the end of

2009 to mid 2011, as excessive

government spending fed an import

surge. As government spending was

cut this import boom burst, and

domestic demand collapsed, taking

the country deep into recession.

3. How To Define Competitiveness?

The issue of competitiveness has

become one generating more heat

than light in debate during the current

crisis. The validity of one

commonplace measure (REERs) widely

used historically has been repeatedly

questioned. In my opinion such

questioning has been largely motivated

by ideological and political motives in

contrast to scientific ones. In fact the

evidence is clear enough.

The REER (or Relative price and cost indicators) aim to assess a country's (or currency area's)

price or cost competitiveness relative to its principal competitors in international markets.

Changes in cost and price competitiveness depend not only on exchange rate movements but

also on cost and price trends. The specific REER for the Sustainable Development Indicators

is deflated by nominal unit labour costs (total economy) against a panel of 36 countries (=

EU27 + 9 other industrial countries: Australia, Canada, United States, Japan, Norway, New

Zealand, Mexico, Switzerland, and Turkey). Double export weights are used to calculate

REERs, reflecting not only competition in the home markets of the various competitors, but

also competition in export markets elsewhere. A rise in the index means a loss of

competitiveness. (Eurostat Definition)

4. Output & Productivity

High output per worker and high wages

are perfectly compatible. The road to

achieve this win-win combination is

through raising productivity, thus

maintaining unit labour costs constant,

or even reducing them.

As can be seen from the accompanying

charts, Germany achieved this combination

between 2000 and 2008, while Italy didn’t. In Italy

productivity stayed pretty much constant while

unit labour costs rose, meaning salaries rose

without the accompanying productivity, while in

Germany unit labour costs stayed constant while

productivity rose. This also gived the lie to the

“cheap German wages” argument, since if wages

hadn’t risen then ULCs would have fallen, which

they only did briefly between 2006 and 2008.

5. The problem in part is that value

added is often a sectorial issue.

For example agriculture and

construction have historically been

low value added and often high

unit labour cost sectors, whereas

petrochemicals or biotechnology

are high value added but also

often low ULC sectors, despite the

fact that wages are higher.

Naturally most societies would like to have a large proportion of high value added activities, and

a comparatively small proportion of low value added ones. But this isn’t as straightforward as it

seems, since the transition from agriculture to biotechnology doesn’t move along what we could

call a smooth production function. Namely you can’t simply transfer workers from one section to

the other. It ain’t that easy. The large number of construction workers recently displaced in Spain

can’t simply move into machine tool manufacturing, for example.

A countries ability to engage in what are high value activities at any moment in time depends on

key factors like the skill, education and experience levels of the workforce, and these change

only slowly. Critically the distribution of these factors depends to some extent on the age

structure of the population.

6. But in part the level of unit labour

costs depends on the level of

international competitiveness, which

in part depends how much of the

economy is in the tradeable sector

and how much in the non-tradeable

part of the economy. By tradeable we

mean in competition with other

producers or service providers

beyond the national frontier.

The key mechanism assumed here is that the tradeable sector, being exposed to external

competition, by definition needs to be more competitive to survive.

So a measure of a country’s lack of international competitiveness isn’t only that exports

are too small, it is also that imports are too big, which is another way of saying that the

domestic tradeable sector isn’t big enough. Normally this loss of competitiveness is

associated with a growing trade and current account deficit, which means the process of

non productivity supported rising living standards can only continue as long as some

external agent is willing to finance it. When confidence that the process is sustainable

subsides, people cease financing, and a crisis occurs. This is what happened to Italy in the

summer of 2011.

7. Export Dependency and International Competitiveness

But now I would like to introduce an additional concept which is generally not accepted

in mainstream economic theory, the idea of export dependent economies. Basically the

idea is that as populations age, demand for credit and with it the rate of increase in

domestic demand wanes. As can be seen in the chart on the right below, household

consumption in Italy surged in the 1990s, and the rate of growth in consumer demand

was quite rapid. The consumer boom was also linked to Italy’s last housing boom. Then

between 2000 and 2007 something changed, and the growth rate slowed. Any internally

coherent macro economic theory needs to be able to explain this change. Then following

the global crisis household consumption slumped, recovered slightly and then slumped

again.

So if we go back briefly to the earlier

chart on the composition of GDP, we

can perhaps formulate a new and

better definition of international

competitiveness, which would be

having an export sector which is

large enough and growing

dynamically enough to produce GDP

growth in an environment where

consumer demand weakens as

populations age.