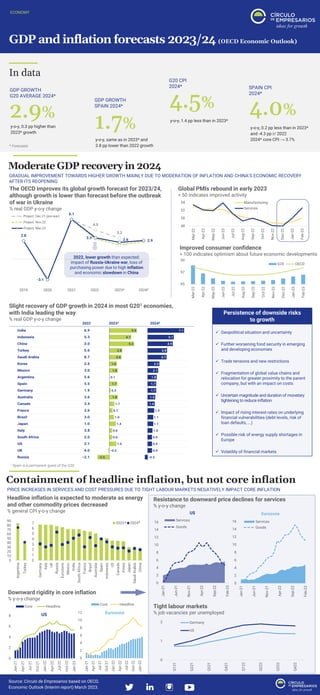

GDP and inflation forecasts Infographic Circulo de Empresarios March 2023

Moderate GDP recovery in 2024 GRADUAL IMPROVEMENT TOWARDS HIGHER GROWTH MAINLY DUE TO MODERATION OF INFLATION AND CHINA'S ECONOMIC RECOVERY AFTER ITS REOPENING The OECD improves its global growth forecast for 2023/24, although growth is lower than forecast before the outbreak of war in Ukraine Global PMIs rebound in early 2023 Improved consumer confidence Slight recovery of GDP growth in 2024 in most G20 economies, with India leading the way Persistence of downside risks to growth Geopolitical situation and uncertainty Further worsening food security in emerging and developing economies Trade tensions and new restrictions Fragmentation of global value chains and relocation for greater proximity to the parent company, but with an impact on costs Uncertain magnitude and duration of monetary tightening to reduce inflation Impact of rising interest rates on underlying financial vulnerabilities (debt levels, risk of loan defaults, ...) Possible risk of energy supply shortages in Europe Volatility of financial markets Containment of headline inflation, but not core inflation PRICE INCREASES IN SERVICES AND COST PRESSURES DUE TO TIGHT LABOUR MARKETS NEGATIVELY IMPACT CORE INFLATION Headline inflation is expected to moderate as energy and other commodity prices decreased Resistance to downward price declines for services Downward rigidity in core inflation Tight labour markets

Recomendados

Recomendados

Más contenido relacionado

Similar a GDP and inflation forecasts Infographic Circulo de Empresarios March 2023

Similar a GDP and inflation forecasts Infographic Circulo de Empresarios March 2023 (20)

Más de Círculo de Empresarios

Más de Círculo de Empresarios (20)

Último

Último (20)

GDP and inflation forecasts Infographic Circulo de Empresarios March 2023

- 1. 48 50 52 54 Mar-22 Apr-22 May-22 Jun-22 Jul-22 Aug-22 Sep-22 Oct-22 Nov-22 Dec-22 Jan-23 Feb-23 Manufacturing Services GDP and inflation forecasts 2023/24 (OECD Economic Outlook) ECONOMY In data Moderate GDP recovery in 2024 Source: Círculo de Empresarios based on OECD, Economic Outlook (Interim report) March 2023. GDP GROWTH G20 AVERAGE 2024* 2.9% y-o-y, 0.3 pp higher than 2023* growth 1.7% GDP GROWTH SPAIN 2024* y-o-y, same as in 2023* and 3.8 pp lower than 2022 growth G20 CPI 2024* 4.5% y-o-y, 1.4 pp less than in 2023* SPAIN CPI 2024* y-o-y, 0.2 pp less than in 2023* and -4.3 pp r/ 2022 2024* core CPI → 3.7% 4.0% GRADUAL IMPROVEMENT TOWARDS HIGHER GROWTH MAINLY DUE TO MODERATION OF INFLATION AND CHINA'S ECONOMIC RECOVERY AFTER ITS REOPENING * Forecasts The OECD improves its global growth forecast for 2023/24, although growth is lower than forecast before the outbreak of war in Ukraine % real GDP y-o-y change Global PMIs rebound in early 2023 > 50 indicates improved activity Improved consumer confidence > 100 indicates optimism about future economic developments Slight recovery of GDP growth in 2024 in most G201 economies, with India leading the way % real GDP y-o-y change Containment of headline inflation, but not core inflation PRICE INCREASES IN SERVICES AND COST PRESSURES DUE TO TIGHT LABOUR MARKETS NEGATIVELY IMPACT CORE INFLATION Headline inflation is expected to moderate as energy and other commodity prices decreased % general CPI y-o-y change Resistance to downward price declines for services % y-o-y change Tight labour markets % job vacancies per unemployed Persistence of downside risks to growth ✓ Possible risk of energy supply shortages in Europe ✓ Geopolitical situation and uncertainty ✓ Further worsening food security in emerging and developing economies ✓ Trade tensions and new restrictions ✓ Fragmentation of global value chains and relocation for greater proximity to the parent company, but with an impact on costs ✓ Uncertain magnitude and duration of monetary tightening to reduce inflation ✓ Impact of rising interest rates on underlying financial vulnerabilities (debt levels, risk of loan defaults, ...) ✓ Volatility of financial markets Downward rigidity in core inflation % y-o-y change 95 97 99 Mar-22 Apr-22 May-22 Jun-22 Jul-22 Aug-22 Sep-22 Oct-22 Nov-22 Dec-22 Jan-23 Feb-23 G20 OECD 0 2 4 6 8 Jan-21 Apr-21 Jul-21 Oct-21 Jan-22 Apr-22 Jul-22 Oct-22 Jan-23 US Core Headline 0 2 4 6 8 10 12 Jan-21 Apr-21 Jul-21 Oct-21 Jan-22 Apr-22 Jul-22 Oct-22 Jan-23 Eurozone Core Headline 0 2 4 6 8 10 12 14 16 Jan-21 Jun-21 Nov-21 Apr-22 Sep-22 Feb-23 US Services Goods 0 2 4 6 8 10 12 14 16 Jan-21 Jun-21 Nov-21 Apr-22 Sep-22 Feb-23 Eurozone Services Goods 0 1 2 Q121 Q221 Q321 Q421 Q122 Q222 Q322 Q422 Germany US 4.5 3.2 2.8 -3.1 6.1 3.3 2.6 2.9 2019 2020 2021 2022* 2023* 2024* Project. Dec.21 (pre-war) Project. Nov.22 Project. Mar.23 2022, lower growth than expected: impact of Russia-Ukraine war, loss of purchasing power due to high inflation and economic slowdown in China 0 1 2 3 4 5 6 7 Germany Italy UK Russia Eurozone Mexico India South Africa France Brazil Australia Spain Indonesia US Canada Korea Japan Saudi Arabia China 2023 2024 0 10 20 30 40 50 60 70 80 90 Argentina Turkey * * 1 Spain is a permanent guest of the G20 2022 2023* 2024*