Connected Home: Video Game Consoles as Entertainment Hubs

•

2 recomendaciones•1,248 vistas

This report examines how consumers are using connected devices in their homes with an emphasis on video game consoles and the efforts of Microsoft, Sony, and Nintendo to position themselves as entertainment hubs in the digital living room of today and the future.

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (12)

Similar a Connected Home: Video Game Consoles as Entertainment Hubs

Similar a Connected Home: Video Game Consoles as Entertainment Hubs (20)

Más de Michael Goodman

Último

Último (20)

Connected Home: Video Game Consoles as Entertainment Hubs

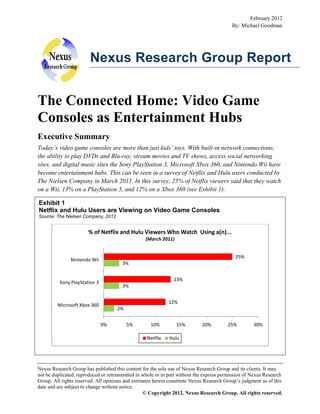

- 1. February 2012 By: Michael Goodman Nexus Research Group Report The Connected Home: Video Game Consoles as Entertainment Hubs Executive Summary Today’s video game consoles are more than just kids’ toys. With built-in network connections, the ability to play DVDs and Blu-ray, stream movies and TV shows, access social networking sites, and digital music sites the Sony PlayStation 3, Microsoft Xbox 360, and Nintendo Wii have become entertainment hubs. This can be seen in a survey of Netflix and Hulu users conducted by The Nielsen Company in March 2011. In this survey, 25% of Netflix viewers said that they watch on a Wii, 13% on a PlayStation 3, and 12% on a Xbox 360 (see Exhibit 1). Exhibit 1 Netflix and Hulu Users are Viewing on Video Game Consoles Source: The Nielsen Company, 2012 % of Netflix and Hulu Viewers Who Watch Using a(n)... (March 2011) 25% Nintendo Wii 3% 13% Sony PlayStation 3 3% 12% Microsoft Xbox 360 2% 0% 5% 10% Netflix 15% 20% 25% 30% Hulu Nexus Research Group has published this content for the sole use of Nexus Research Group and its clients. It may not be duplicated, reproduced or retransmitted in whole or in part without the express permission of Nexus Research Group. All rights reserved. All opinions and estimates herein constitute Nexus Research Group’s judgment as of this date and are subject to change without notice. © Copyright 2012. Nexus Research Group. All rights reserved.

- 2. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Microsoft, Sony and Nintendo have taken different approaches to developing their consoles as home entertainment systems. Microsoft embraced digital distribution early on, while Sony has sought to straddle the line between physical distribution (e.g., Blu-ray) and digital distribution (e.g., PlayStation Movie Store). And Nintendo, in a departure from the past, is beginning to embrace the console as a home entertainment system with the integration of Netflix and the iBBC Player, but is taking a more conservative approach than either of its competitors. This Report, examines how consumers are using connected devices in their homes with an emphasis on video game consoles and the efforts of Microsoft, Sony, and Nintendo to position themselves as entertainment hubs in the digital living room of today and the future. 2 © Copyright 2012. Nexus Research Group. All rights reserved.

- 3. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Contents I. Introduction .......................................................................................................................................... 3 II. Impact of In-Home Connected Devices ................................................................................................ 4 III. Video Game Consoles as Home Entertainment Systems ...................................................................... 8 Console Activities ................................................................................................................................. 8 Time Spent by Activities ...................................................................................................................... 10 IV. Netflix and Hulu Come to the Console ............................................................................................... 15 VI. Conclusions and Recommendations ................................................................................................... 18 Conclusions......................................................................................................................................... 18 Recommendations ............................................................................................................................... 19 I. Introduction That consumption of on-demand movies, music and games is growing should come as no surprise to anyone. However, the speed at which demand has grown for these applications and services and the amount of bandwidth they consume is suprising. According to Sandvine (a network management company), real-time entertainment (applications and protocols that allow “on-demand” entertainment that is consumed as it arrives) as a percentage of fixed network traffic during the peak period (4pm 11pm) has grown at an average annual rate of 41% over the past three years. In 2009, real-time entertainment accounted for 29.5% of fixed network traffic in North America between 4pm and 11pm; by 2011 it had grown to over half (53.6%). Nor is this growth pattern entiely unique to North America. The Asia-Pacific region has seen peak period usage of real-time entertainment grow from 26.3% of fixed network traffic in 2009 to 49.0% in 2011; an average annual growth rate of 36.5%. Europe, however, has not seen as dramatic a rise. In 2009, peak period usage of real-time entertainment accounted for 30.4% of fixed network traffic. By 2011 it had grown to 33.2%; an average annual growth rate of 4.5%. Real-Time Entertainment: Applications and protocols that allow “on-demand” entertainment that is consumed (viewed or heard) as they arrive. This includes streamed or buffered audio (Pandora, Rdio) and video (RTSP, RTP, RTMP, Flash, MPEG), peercasting (PPStream, Octoshape), placeshifting (Slingbox), and specific streaming sites and services (Netflix, NCAA, Hulu, YouTube, Google Video, Spotify, BBC iPlayer). Secure Tunneling: Encrypted tunnels typically used for Virtual Private Networks and secure web transactions. Real-Time Communications: Applications and protocols that allow interactive chat, voice, and video communications. Bulk Entertainment: Entertainment that is acquired in bulk then consumed sometime after arrival such as movie download services. 3 © Copyright 2012. Nexus Research Group. All rights reserved.

- 4. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Exhibit 1 Fixed Network Traffic Composition During Peak Period (4pm - 11pm) Source: Sandvine Global Internet Phenomena Report, 2012 Top 5 Applications/Protocals During Peak Period (North America, Fixed Networks) 150.0% 100.0% 50.0% 9.8% 4.0% 15.1% 2.3% 29.5% 38.7% 0.0% 2009 Web Browsing P2P Filesharing Storage & Back-up Services Real-Time Communications Gaming 12.1% 3.1% 19.2% 2.7% 9.4% 3.8% 14.3% 42.7% 53.6% 20.2% 16.6% 2010 2.3% 2011 Real-Time Entertainment Secure Tunneling Bulk Entertainment Social Networking All Other Traffic Driving much of this growth is Netflix. With 21.6 million streaming accounts in 4Q 2011, Neftlix accounted for 32.7% of downstream Internet traffic during North American peak home Internet usage hours (4pm - 11pm). Think about what would happen to download speeds if the other roughly 100 million TV households in North America started using Netflix streaming. II. Impact of In-Home Connected Devices Driving much of this growth has been the influx of connected devices. According to Sandvine, 55% of real-time entertainment is consumed on the television (either directly to a connected TV or indirectly via a game console, Blu-ray player or connected media player), a mobile device or tablet. The remaining 45% is consumed on desktop and laptop computers, with some of this being forward to the TV. In 2009, the global installed base of in-home connected devices was nearly 64 million. Due to of more connected devices entering the market, connectivity becoming a basic feature on a greater number of devices, and services taking advantage of this connectivity, the installed base of in-home connected devices grew to 319 in 2011. By 2016, Nexus Research Group anticipates that the installed base of in-home connected devices will grow to 1.5 billion (see Exhibit 2 & 3). For more detail on the growth of in-home connected devices, see the Nexus Research Group report The Connected 4 © Copyright 2012. Nexus Research Group. All rights reserved.

- 5. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Home: Battle for Dominance in the Digital Living Room and corresponding 2012 In-Home Connected Device Forecast. In the early stages, North America has been leading the growth of in-home connected devices. In 2009, North America accounted for 40% of the global installed base of in-home connected devices followed by Western Europe with 31% and the Asia-Pacific region with a 22% share. By 2011, North America still accounted for the largest of the global installed base of in-home connected devices (35%) but the Asia-Pacific region was gaining and had tied Western Europe’s market share (27%). By 2016, driven by growing economies in China and India, and a seemingly insatiable demand for consumer electronics in Japan and South Korea the Asia Pacific regions share of in-home connected devices will grow to 31% in 2016, edging out North America (30%) and Western Europe (26%). Exhibit 2 By 2016 the Installed Base of In-Home Connected Devices will Reach 1.5 Billion Source: DFC Intelligence, 2012 Global Installed Base of In-Home Connected Devices 1,600 1,400 Units (in Millions) 1,200 1,000 800 600 400 200 0 2009 Connected TVs 2010 2011 Blu-ray Players 2012 2013 Video Game Consoles 2014 2015 2016 Connected Media Players 5 © Copyright 2012. Nexus Research Group. All rights reserved.

- 6. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Exhibit 3 By 2016 the Installed Base of In-Home Connected Devices will Reach 1.5 Billion Source: Nexus Research Group, 2012 Year Connected TVs Blu-Ray Players Video Game Consoles Connected Media Players Cumulative Total 2009 22.1 ----- 41.8 ----- 63.9 2010 62.2 23.1 84.1 2.0 171.3 2011 129.3 58.0 123.7 8.4 319.3 2012 207.7 107.2 162.3 15.7 493.0 2013 304.6 175.9 206.0 24.9 711.4 2014 427.0 255.9 250.1 36.0 969.0 2015 565.8 342.4 295.8 49.4 1,253.4 2016 724.4 432.7 339.7 64.6 1,561.4 Because of their installed base, likelihood of being connected, and partnerships with content owners, video game consoles have become important drivers of over-the-top content. Established installed base. In 2011, there were 146 million current generation consoles (PlayStation 3, Xbox 360 and Wii) in consumer’s homes worldwide (see Exhibit 4, & 5). By 2016, Nexus Research Group estimates that the global installed base of video game consoles will grow to 170 million. Users are taking advantage of connectivity. Not only is there a significant installed base of video game consoles but unlike other internet-ready devices, which may offer connectivity as a feature but are not actually connected to the internet, a significant number of video game consoles are connected. In 2011, 39% of the global installed base of video game consoles were connected, by 2016, this will grow to 44%. Even this however does not tell the complete story. Among the current generation of consoles, the Sony PlayStation 3 and Microsoft Xbox 360 have taken a much more aggressive approach to connectivity than the Nintendo Wii. While all three consoles are internet-ready Sony and Microsoft have pushed connected applications and content, such as online gaming, video, music and social media, much harder than Nintendo. As a result, the PlayStation 3 and Xbox 360 are more likely than the Wii to be connected. When it comes to connectivity, the Xbox 360 is king. In 2011, Nexus Research Group estimates that 57% of the Xbox 360 global installed base were connected to Xbox Live (Microsoft’s online service for the Xbox 360). In comparison, 47% of the PlayStation 3 were connected and only 23% of Wii’s were connected. Future generations of consoles are more likely to be connected. Nexus Research Group estimates that more than half (51%) of next generation consoles (Nintendo Wii U, Microsoft Xbox 720, and PlayStation 4) be physically connected, with this likely increasing in the later stages of their product lifecycle. 6 © Copyright 2012. Nexus Research Group. All rights reserved.

- 7. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Geography is also a contributing factor to console connectivity. In 2011, 65% of both the Xbox 360 and PlayStation 3 installed base was connected in North America. In comparison, 55% of the Western European Xbox 360 installed base was connected and 30% of the Japanese installed base. Among the PlayStation 3 installed base in Japan 40% was connected, while 30% of the Western European installed base was connected. Content options available on video game consoles is growing. Content owners and aggregrators are embracing the video game console as a distribution partner. In October 2011, Microsoft announced a significant expansion in the number of content providers available on the Xbox 360. Over 40 global media partners (representing various regions of the world) have been added include ESPN, EPIX, HBO, Hulu/Hulu Plus, LOVEFiLM, Telefónica España – Movistar Imagenio, AlloCiné, Crackle, CinemaNow, Bravo, HBO, BBC, Rogers on Demand and Telenovelas/Sports (Televisa). Exhibit 4 Installed Base of Connected Consoles Source: DFC Intelligence, 2012 Global Video Game Console Installed Base 200.0 180.0 160.0 Units (in Millions) 140.0 120.0 100.0 80.0 60.0 40.0 20.0 0.0 2010 2011 2012 Console Installed Base 2013 2014 2015 2016 Connected Consoles 7 © Copyright 2012. Nexus Research Group. All rights reserved.

- 8. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Exhibit 5 Installed Base of Connected Consoles Source: Nexus Research Group, 2012 Console Installed Base Year Connected Consoles % of Installed Base Connected 2010 136.6 48.9 36% 2011 146.0 57.1 39% 2012 157.3 63.5 40% 2013 167.6 71.1 42% 2014 176.1 75.0 43% 2015 181.1 78.3 43% 2016 185.4 81.0 44% III. Video Game Consoles as Home Entertainment Systems At its most basic level, the entertainment ecosystem is comprised of three primary components (for a more in-depth examination of the entertainment ecosystem see Nexus Research Group Report - The Connected Home: Battle for Dominance in the Digital Living Room): Content. This includes things such movies and TV shows, music, games, user generated content and apps. Distribution. Distribution is defined as how consumers access content and include electronic distribution over managed and unmanaged networks, broadcasting, and physical distribution through brick-n-mortar retailers. Device. Finally, require require some kind of device to consume the content on. This includes (but are not limited to) TVs, set-top boxes, video game consoles, PCs, smartphones and tablets. Console Activities Microsoft (via Xbox Live), Sony (via the PlayStation Network) and to a lesser degree Nintendo have built an ecosystem that includes all of the components required to be a viable distribution channel for movies and TV shows, music and games. The last requirement for success is consumer adoption and early results indicate that video game consoles are off to a strong start establishing themselves as home entertainment hubs. Not surprisingly, considering it is a gaming console after all, gaming it the top activity among console users age 13+, according to a survey conducted by The Nielsen Company in 2010 (see Exhibit 6). Detailed examination of usage patterns by console, however, yields unique user profiles. Eighty-seven percent of both Xbox 360 and Wii users age 13+ said they had played video games on the respective console, while 80% had done on the PlayStation 3. The vast majority of this game play 8 © Copyright 2012. Nexus Research Group. All rights reserved.

- 9. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 was offline, but just over half (54%) of Xbox 360 users and 45% of PlayStation 3 users said that they play games online. In comparison, only 27% of Wii users age 13+ play games online. Given the emphasis both Sony and Microsoft place on online game play, these results are not surprising. After gaming, watching video is the next most popular activity on video game consoles. Video consumption comes in a number of forms on video game consoles, including streaming, downloading and watching physical media (DVDs and Blu-ray disks). Physical media (DVDs and Blu-ray disks) is the most popular format for video on both the PlayStation 3 and Xbox 360. According to The Nielsen Company, 72% of PlayStation 3 users age 13+ said they had watched a DVD or Blu-ray movies on the PlayStation 3 and 43% of Xbox 360 users age 13+ said they had watched a DVD or Blu-ray movieson the Xbox 360. (Please note that the Xbox 360 does not support Blu-ray and the Wii does not support video playback from either DVD or Blu-ray) After physical media, streaming is the next most popular method for watching video on a console. Twenty-six percent of Xbox 360 users age 13+ said they watch VOD/subscription streaming services (e.g., Netflix, Hulu Plus, LOVEFiLM) on their Xbox 360, followed by 23% of both PlayStaion 3 users and Wii users. Downloading is nearly as popular with 22% of Xbox 360 users age 13+ and 21% of PlayStation 3 users age 13+ saying that they had watched downloaded movies or TV shows on their respective console. (Please note that the Wii does not have a hard drive, negating the ability to download content) Exhibit 6 % of Users* Age 13+ Who Do Each Activity Source: The Nielsen Company, 2012 % of Users* Age 13+ Who Do Each Activity 87% 80% 87% 81% 72% 75% Play Video Games (Net) Play Video Games Offline 27% Play Video Games Online Watch DVDs/Blu-Ray 72% 43% 23% 23% 26% Watch VOD/Streaming Subscription Service Listen to CDs, MP3s or other Music (Online or … 8% Watch Downloaded Movies or TV Shows 0% 23% 23% 21% 22% 20% 27% 20% Use Internet for Browsing, Social Networking… Wii 46%54% 20% PlayStation 3 40% 60% 80% 100% Xbox 360 9 © Copyright 2012. Nexus Research Group. All rights reserved.

- 10. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 * User is defined as someone who owns the console and uses at least one of these features (October 2010) Music, web browsing and social networking are also popular activities on video game consoles. Twenty-three percent of both Xbox 360 and PlayStation 3 users age 13+ listen to CDs, MP3s or other music (online or purchased) on their respective console. Music consumption is less popular on the Wii with only 8% of users reporting that they listen to music. Twenty-seven percent of PlayStation 3 users age 13+ use their console for web browsing, social networking and watching video (user generated) followed by 20% of Xbox 360 and Wii users. Time Spent by Activity Microsoft Xbox 360 Examining activities by time spent yields distinct usage patterns for each console. According to Nielsen, despite all the non-gaming content available on the Xbox 360, users age 13+ spend the majority of their console time (67%) playing games, up 8% YoY (see Exhibit 7). Xbox 360 users age 13+ are also far more likely to engage in online game play than users of the PlayStation 3 or Wii. Thirty-three percent of Xbox 360 users age 13+ console time was spent playing games online compared to 16% of PlayStation 3 users and 8% of Wii users. Exhibit 7 Share of Console Time Among Xbox 360 Users* Age 13+ Source: The Nielsen Company, 2012 Share of Console Time Among Xbox 360 Users* Age 13+ 34% 34% Play Video Games Offline 28% Play Video Games Online 10% Watch VOD/Streaming Services Watch DVDs/Blu-Ray 9% Watch Downloaded Movies/TV Shows All Other (Brows Web, Listen to Music, Other) 33% 14% 11% 6% 5% 11% 5% 0% 20% 2010 40% 2011 10 © Copyright 2012. Nexus Research Group. All rights reserved.

- 11. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 * User is defined as someone who owns the console and uses at least one of these features (October 2010 and 2011) It should be noted that this data was collected prior to Microsoft’s redesign of the Xbox 360’s user interface which made it easier to discover movies, TV shows, music, and social networking apps as well as the expansion of these offerings which began in late 2011 and continues through 2012. According to Microsoft, prior to its latest update in the fall of 2011, 40% of all Xbox activity was non-game. This translated to an average of 30 hours of video consumption per month per Xbox. Overall, global video consumption on Xbox LIVE increased 140% from CY 2010 to CY 2011. Overall, time spent on non-gaming activities by Xbox 360 users fell by 13% YoY, from 38% of console time in October 2010 to 33% in October 2011. The majority of this decline was in the “Other” category that included listening to music, web browsing, social media and any other miscellaneous applications and services. In 2011, video (DVDs, streamed and downloads) accounted for 85% of Xbox 360 users age 13+ console time spent on non-gaming activities, up 19% YoY. Watching video-on-demand (VOD)/streaming services saw the most grow in the video category. Growing 40%, from 10% of console time spent in October 2010 to 14% of console time spent in October 2011. Given the improvements to the Xbox’s user interface and expanded content offerings it is likely that 2012 will see time spent on the non-gaming activities grow. Sony PlayStation 3 While the Xbox 360 appeals most strongly to hardcore gamers, the PlayStation 3, primarily due to the inclusion of Blu-ray, has a more diversified usage profile. According to the Nielsen study, gaming accounts for 54% of console time among PlayStation 3 users age 13+, up 10% YoY (see Exhibit 8). Whereas online and offline game play is evenly split among Xbox 360 users, PlayStation 3 users age 13+ show a clear preference for offline game play. In 2012 offline game play accounted for 38% of PlayStation 3 users age 13+ console time, up nearly 27% YoY. Online play declined nearly 16%, from 19% of console time spent in 2010 to 16% in 2011. Among PlayStation 3 users age 13+ console time spent on non-gaming activities fell nearly 10% YoY, from 51% of console time in October 2010 to 46% in October 2011. Like Xbox 360 users, the majority of this decline was in the “Other” category that included listening to music, web browsing, social media and any other miscellaneous applications and services. In 2011, video (DVDs, streamed and downloads) accounted for the vast majority (91%) of PlayStation 3 users age 13+ console time spent on non-gaming activities, up 16% YoY. Watching DVDs/Blu-ray is the most popular non-gaming activity among PlayStation users age 13+, accounting for 22% of their console game time, followed by watching video-on-demand (VOD)/streaming services (15%). The success of Blu-ray on the PlayStation 3 has been critical to Sony as the PlayStation 3 accounts for roughly two-thirds of the Blu-ray player installed base, however, streaming video is beginning to cut into Blu-ray viewing. According to the Nielsen study, console time spent watching DVDs/Blu- 11 © Copyright 2012. Nexus Research Group. All rights reserved.

- 12. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 ray fell 19% YoY, from 27% of console time spent in October 2010 to 22% of console time spent in October 2011. This trend, if it continues, is troubling to both Sony (corporate) and the movie studios who hoped that Blu-ray would replace the roughly $20 billion in revenue that DVDs once produced. Exhibit 8 Share of Console Time Among PlayStation 3 Users* Age 13+ Source: The Nielsen Company, 2012 Share of Console Time Among PlayStation 3 Users* Age 13+ 30% Play Video Games Offline Play Video Games Online 16% 9% Watch VOD/Streaming Services 19% 15% Watch DVDs/Blu-Ray 22% Watch Downloaded Movies/TV Shows All Other (Brows Web, Listen to Music, Other) 38% 27% 4% 5% 11% 4% 0% 20% 2010 40% 2011 * User is defined as someone who owns the console and uses at least one of these features (October 2010 and 2011) Nintendo Wii While the majority of console time spent by Wii users age 13+ is playing offline games, streaming video usage is surprisingly strong as well. According to the Nielsen study, gaming accounted for 66% of Wii users age 13+ console time in October 2011. Of this, offline game play accounted for 87% of their time spent playing games. In October 2011, 8% of Wii users console game time was spent playing games online, a decline of 33% from 12% in October 2010. Among Wii users age 13+, console time spent on non-gaming activities grew 19% YoY, from 31% of console time in October 2010 to 37% in October 2011. Driving this growth is consumption of video. This is surprising since Nintendo did not design the Wii to be an entertainment hub. The Wii lacks the ability to playback DVDs or Blu-ray disks and does not have a hard drive that movies or TV show can be downloaded to. What you can do is watch video-on-demand (VOD)/streaming services, and this category grew 65% YoY, from 20% of Wii users console time in October 2010 to 33% in October 2011. 12 © Copyright 2012. Nexus Research Group. All rights reserved.

- 13. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Exhibit 9 Share of Console Time Among Wii Users* Age 13+ Source: The Nielsen Company, 2012 Share of Console Time Among Wii Users* Age 13+ 57% 55% Play Video Games Offline Play Video Games Online 12% 8% 20% Watch VOD/Streaming Services Watch DVDs/Blu-Ray Not Applicable Watch Downloaded Movies/TV Shows 33% Not Applicable All Other 4% 11% 0% 20% 2010 40% 60% 2011 * User is defined as someone who owns the console and uses at least one of these features (October 2010 and 2011) Clearly all three consoles have established themselves as viable alternative for movies and TV shows, what is surprising in the degrees of success. Despite aspiring to be an entertainment hub Microsoft still has a ways to go with only 28% of Xbox 360 users console time spent on video (see Exhibit 10). However, with its revamped user interface, significantly more content partners, and voice activated search through Kinect we are likely to see video consumption grow among Xbox 360 users. Though, video usage accounts for the smallest percentage of time among Xbox users, compared to the PlayStation 3 and Wii, it is the most profitable as most, if not all, video services require users to have a Gold subscription to Xbox Live ($59.99 annually). Plus the cost to download a movie or TV show or subscribe to a streaming service. Equally surprising is the strength of Nintendo in the video category. Though you cannot play DVDs or Blu-ray disks or download movies or TV show to the Wii, Wii users still spent a third (33%) of their console time watching video, 18% more than Xbox 360 users. Though Nintendo did not design the Wii to be an entertainment hub the addition of Netflix has clearly had a significant impact on the Wii. Also helping the Wii establish itself as a video platform is its position in the household. 13 © Copyright 2012. Nexus Research Group. All rights reserved.

- 14. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 According to Nielsen, the Wii is the console most likely to be found in living / family room making it available to a wide range of family members. Exhibit 10 Share of Console Time Among PlayStation 3 Users* Age 13+ Source: The Nielsen Company, 2012 Share of Time Spent Watching Video Among Console Users* Age 13+ 60% 40% 5% 5% 9% 22% 14% 15% Xbox 360 20% PlayStation 3 33% 0% Watch VOD/Streaming Services Watch DVDs/Blu-Ray Wii Watch Downloaded Movies/TV Shows * User is defined as someone who owns the console and uses at least one of these features (October 2011) As a game console the PlayStation 3 seems to have lost something, particularly when compared to its predecessors, but as a home entertainment system the PlayStation is clearly hitting its stride with PlayStation 3 users spending nearly as much time with non-game activities, particularly video, as gaming. Overall, PlayStation 3 users spent 50% more console time watching video than Xbox users and 27% more than Wii users. 14 © Copyright 2012. Nexus Research Group. All rights reserved.

- 15. The Connected Home: Video Game Consoles as Entertainment Hubs IV. February 2012 Netflix and Hulu Come to the Console As evidenced in the previous section video game console are emerging as important platforms for video distribution but what impact will they have on individual providers’ distribution plans. For at least one video provider, Netflix, video game consoles have emerged as an important distribution channel. According to a survey of 12,000 U.S. Hulu and Netflix users in March 2011 by the Nielsen Company, video game consoles were the top device for accessing Netflix. Fifty percent of Netflix subscribers surveyed said that they use a video game console to watch Netflix. This was followed by watching directly on a computer (42%) and watching on a computer connected to a TV (14%) (see Exhibit 11). In comparison, Hulu, though available on all three video game consoles (same as Netflix), saw only 8% of its user’s say that they watch on a game console. Hulu users are much more likely to watch directly on a computer (89%) or on a computer connected to a TV. Exhibit 11 How are Netflix and Hulu Users Watching? Source: The Nielsen Company, 2012 % of Netflix and Hulu Viewers Who Watch Using a(n)... (March 2011) Computer Directly 89% 42% 14%20% Computer Connected to TV 8% Video Game Console 50% 3% 5% 2% 3% Roku Box Mobile Phone 2%6% 2% 11% Connected TV Internet-Connected Blu-ray Player iPad 1% 3% TiVo w/Netflix Access 2% 1% 1% 1% 1% Apple TV Google TV 0% 10% 20% Hulu 30% 40% 50% 60% 70% 80% 90% 100% Netflix Now a large part of the discrepancy between Hulu and Netflix usage on video game consoles is attributable to differing business models. Netflix content is only available via subscription ($7.99 per 15 © Copyright 2012. Nexus Research Group. All rights reserved.

- 16. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 month), however, subscribers can access movies and TV shows across multiple devices (video game consoles, connected TVs, iPads, connected media players, Blu-ray players, etc.). In contrast, Hulu has both a free ad-supported service and a more robust subscription service ($7.99 per month), however, only the subscription service is available via video game console. In addition to having different business model the way consumers use Netflix and Hulu differ as well. Netflix users are more well rounded; consuming both movies and television shows. According to Nielsen, 53% of Netflix users watch both movies and television shows, 36% watch movies only and 11% watch TV shows only (see Exhibit 12). In comparison, the vast majority of Hulu users (73%) only watch TV shows, 18% only watch movies while 9% watch both movies and TV shows. Exhibit 12 What are Netflix and Hulu Viewers Watching? Source: The Nielsen Company, 2012 % of Netflix and Hulu Viewers Who Watch... (March 2011) 36% Movies 18% 11% TV Shows 73% 53% Both Equaly 9% 0% 20% 40% Netflix 60% 80% Hulu The different usage profiles for Hulu and Netflix is significant as it indicates the need for video providers to differentiate in some way. Many of the video providers available on the Xbox Live (Netflix, Hulu Plus, Crackle, Vudu, CinemaNow) offer very similar content making it difficult for them to breakout from the pack. Particularly since Netflix, with its high brand recognition and large subscription base is available on all the consoles. Video providers offering movies and TV shows must find a way to carve out their own niche or be content with the crumbs left behind by larger providers like Netflix. 16 © Copyright 2012. Nexus Research Group. All rights reserved.

- 17. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Some ways to do this include the following. Use marketing promotions. In the UK, Blinkbox is collaborating with Domino’s Pizza to promote themed movie packages that provides customers with a 40% discount when they spend £25 or more at Domino’s Pizza. Combine physical and digital media. In the UK, Tesco (a grocery and general merchandise retailer) and Blinkbox (Tesco owns 80% of Blinkbox) rewards customers who buy physical DVDs and Blu-rays in-store with online access to the same movie on Blinkbox. Since rolling out this initiative, Blinkbox has seen its monthly online sales double. Focus on the high-end, early adopter. While not quite up to the quality of Blu-ray, Vudu's high-quality HDX format significantly outperforms standard DVDs, and at least comes close to the video quality of Blu-ray. In addition, Vudu was also the first online video service to offer 3D video, though not surprisingly the selection is limited. 17 © Copyright 2012. Nexus Research Group. All rights reserved.

- 18. The Connected Home: Video Game Consoles as Entertainment Hubs VI. February 2012 Conclusions and Recommendations Conclusions While many in-home connected devices (such as connected TVs, Blu-ray players and connected media players) are entering the market none can claim to be having the same impact as video game consoles. This can be seen in Exhibit 1, which shows 25% of Netflix users watch on a Nintendo Wii. While competition from other devices is sure to increase in the next several years it is unlikely that video game consoles will recede into the background. Rather they will continue to add new capabilities (such as Xbox 360’s voice search) and additional content and grow. Additional insights include the following: Connected devices are driving the growth on real-time entertainment. According to Sandvine (a network management company), 55% of real-time entertainment is consumed on the television (either directly to a connected TV or indirectly via a game console, Blu-ray player or connected media player), a mobile device or tablet. The remaining 45% is consumed on desktop and laptop computers, with some of this being forward to the TV. The global installed base of video game consoles continues to grow. In 2011, there were 146 million current generation consoles (PlayStation 3, Xbox 360 and Wii) in consumer’s homes worldwide (see Exhibit 4, & 5). By 2016, Nexus Research Group estimates that the global installed base of video game consoles will grow to 170 million. Unlike other in-home connected devices, consumers are actually using the connectivity in video game consoles. While many devices are network capable, it does not mean that consumers are actually connecting them to their home network or use them to access online content. This however, is not the case with video game consoles. In 2011, 39% of the global installed base of video game consoles were connected, by 2016, this will grow to 44%. Xbox is the top console for connectivity. Nexus Research Group estimates that 57% of the Xbox 360 global installed base are connected to Xbox Live (Microsoft’s online service for the Xbox 360). In comparison, 47% of the PlayStation 3 are connected and only 23% of Wii’s are connected. Geography is a contributing factor to console connectivity. In 2011, 65% of both the Xbox 360 and PlayStation 3 installed base was connected in North America. In comparison, 55% of the Western European Xbox 360 installed base was connected and 30% of the Japanese installed base. Among the PlayStation 3 installed base in Japan 40% was connected, while 30% of the Western European installed base was connected. The number of content options available on video game consoles is growing. Content owners and aggregrators are embracing the video game console as a distribution partner. The PlayStation 3 is a true entertainment hub. More than any other console, PlayStation 3 users split their console time evenly between gaming and non-gaming activities. Gaming 18 © Copyright 2012. Nexus Research Group. All rights reserved.

- 19. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 accounts for 54% of console time among PlayStation 3 users age 13+ while non-gaming activities account for 46% of their console time. Recent updates make the Xbox 360 a more formidable entertainment hub. While nongaming activities have lagged on the Xbox 360 (compared to the PlayStation 3 and Wii), improvements to its user interface and expanded content offerings make it likely that 2012 will see time spent on the non-gaming activities, particularly video, grow significantly. Streaming, particularly on game consoles is having a negative influence on Blu-ray. The success of Blu-ray on the PlayStation 3 has been critical to Sony as the PlayStation 3 accounts for roughly two-thirds of the Blu-ray installed base, however, streaming video is beginning to cut into Blu-ray viewing. This trend, if it continues, is troubling to both Sony (corporate) and movie studios who hoped that Blu-ray would replace the roughly $20 billion in revenue that DVDs once produced. Recommendations Discovery must improve. Regardless of the device if you don’t know the programming is available or can’t find it, you can’t view it. Currently it is difficult to discover movies and TV shows if you are not specifically searching for it. This must improve. Video providers must differentiate themselves from each other. Too a large extent, video providers are much of the same content. This gives Netflix with its large subscriber base and high brand awareness a large advantage. Whether it is through promotions, exclusive rights, unique business models, or niche offerings, just to name a few, video providers must find ways to differentiate themselves from the competition. Simplify the registration process. If the registration process is too complicated or requires too many steps consumers will just abandon the process. There are lots of other video services with similar content. For example, the registration for Crackle on the Xbox 360 is a two step process requiring you to register on both Xbox Live and online. Don’t forget about customer care. You never get a second chance to make a first impression and nowhere can you make a bigger impression than with excellent customer care. This should include email and instant help through chat and telephone support. In addition, companies should also publish a comprehensive FAQs and help page online. Combine physical and digital media. In the UK, Tesco (a grocery and general merchandise retailer) and Blinkbox (Tesco owns 80% of Blinkbox) rewards customers who buy physical DVDs and Blu-rays in-store with online access to the same movie on Blinkbox. Since rolling out this initiative, Blinkbox has seen its monthly online sales double. Offer movies that will appeal to the high-end, early adopter. While not quite up to the quality of Blu-ray, Vudu's high-quality HDX format significantly outperforms standard DVDs, and at least comes close to the video quality of Blu-ray. In addition, Vudu was also the first online video service to offer 3D video, though not surprisingly the selection is limited. 19 © Copyright 2012. Nexus Research Group. All rights reserved.

- 20. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 20 © Copyright 2012. Nexus Research Group. All rights reserved.

- 21. The Connected Home: Video Game Consoles as Entertainment Hubs February 2012 Conditions of Purchase Purchase of this multi-client study is on a nonexclusive basis. This study has not been commissioned or contracted for by any one person or organization. The information contained is confidential to the purchaser, and the purchaser agrees not to circulate or loan the study in whole or in part to: their subsidiaries or divisions, industry trade associations (if not the purchaser), the general public, the media, nor other parties not belonging to their company, agency or organization. Unauthorized reproduction and dissemination which is discovered by Nexus Research Group (the publisher) shall constitute grounds for legal prosecution and damages under U. S. copyright law. Nexus Research Group has made every attempt to verify the accuracy and completeness of information in this study from sources we believe to be reliable. It is understood, however, that our estimates, forecasts, opinions and recommendations represent the judgment of our analysts, based on the best information available at the time of publication. It is recommended that purchasers also consult other available business sources and not rely solely on this analysis as the basis for major strategic, financial, or management decisions. Nexus Research Group makes no warranty or representation, either expressed or implied, with respect to the information in this report. In no event will Nexus Research Group be liable for direct, indirect or consequential damages resulting from any defect or inaccuracy in this report, even if advised of the possibility of such damages. Information about specific companies is not intended to be a complete description, nor of their securities, nor is this study an offer to buy or sell such securities. Nexus Research Group’s liability, if any, shall not exceed the amount paid for this study. About This Report This report is part of a series of reports on Advertising and Games. The focus of this report is on the overall industry. Other reports have more detailed analysis of companies, business models, trends and breakouts of individual segments like advertising in and around console / PC games or social / casual games.. The reports in this Advertising and Games series, including this report, are based on a review of historical trends and opinions of leading members of the video game industry, including analysts, consultants, developers, publishers, retailers and consumers. This report has been prepared by utilizing a variety of primary and secondary research techniques including: telephone and personal interviews; analysis of market surveys, trade journals and company literature; extensive database searches; and Nexus Research Group’s original compilations and analysis. A Nexus Research Group report is more than a collection of raw statistics. We carefully scrutinize and analyze data from a variety of sources. The result is a comprehensive overview that puts facts and figures in context. Anyone who has attempted to collect figures for the online game industry knows that is difficult to obtain accurate statistics. We have studied market surveys, investment analyst reports and other sources of industry information. Our statistics and forecasts are based on the careful analysis of the available research, a great deal of which is contradictory. In many cases, we made assumptions based on the best available information. We feel our figures accurately reflect past and future market conditions. At the very least, these numbers track the industry trends and accurately estimate the market share of the various players. 21 © Copyright 2012. Nexus Research Group. All rights reserved.