Ifs30 schedul

•Descargar como PPT, PDF•

1 recomendación•543 vistas

Indian financial system

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (19)

Destacado

Similar a Ifs30 schedul

Similar a Ifs30 schedul (20)

Último

Último (20)

Ifs30 schedul

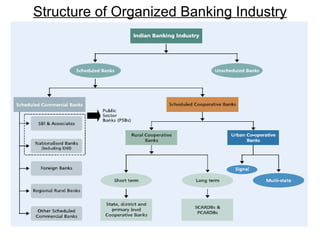

- 1. Structure of Organized Banking Industry

- 2. Scheduled Banks • A bank that is listed under the second schedule of the RBI Act, 1934. • Fulfills conditions: 1) Has a paid up capital and reserves of at least 0.5 million. 2) Its affairs are not being conducted in a manner prejudicial to the interests of its depositors. • Every Scheduled bank enjoys the following facilities. 1) Such bank becomes eligible for debts/loans on bank rate from the RBI 2) Such bank automatically acquire the membership of clearing house. • They are classified into commercial and cooperative banks. • Basic difference between the two is in their holding pattern. Scheduled cooperative banks are cooperative credit institutions that are registered under the Cooperative Societies Act.

- 3. Scheduled Banks • Schedule commercial banks are further classified into: 1) Public Sector Banks- . Nationalised banks (10) and SBI and associates (7), together form the public sector banks group and control around 70% of the total credit and deposits businesses in India. 2) Foreign Banks- are present in the country either through complete branch/subsidiary route presence or through their representative offices. • Regional Rural Bank- represents the cooperative specialty of local orientation and the sound resource base of commercial banks. Equity holding is jointly held by the central government, the concerned state government and the sponsor bank in the ratio 50:15:35. • Scheduled cooperative banks are further classified into urban credit cooperative institutions and rural cooperative credit institutions.

- 4. Non Schedule Banks • Banks which are not included in the second schedule of RBI Act, 1934. • Total Bank share capital is less than five lakhs. • They are not governed according to the RBI Act and they receives no benefits from the RBI. The banks have no place in the list of recognized banks of the RBI. • Functions in the form of Local Area Banks (LAB) with jurisdiction over a maximum of three contiguous districts. • Aim is to aid in the mobilisation of funds of rural and semi urban districts.

- 5. Sources of Income 1. Interest earned from loans given to customers. 3. Money derived from the commission owners of current accounts. 5. Agency services render to customers. 7. Amount accrue to commercial banks from discounting of bills of exchange. 9. Amount from capital investments which yield profits. 11. Money through the sale of government's treasury bills and shares for companies.