11.vol. 0002www.iiste.org call for paper no. 2_c reinig & ca tilt _pp176-197

•

3 recomendaciones•576 vistas

Recomendados

Recomendados

Más contenido relacionado

La actualidad más candente

La actualidad más candente (13)

Destacado

Destacado (13)

Similar a 11.vol. 0002www.iiste.org call for paper no. 2_c reinig & ca tilt _pp176-197

Similar a 11.vol. 0002www.iiste.org call for paper no. 2_c reinig & ca tilt _pp176-197 (20)

Más de Alexander Decker

Más de Alexander Decker (20)

Último

Último (20)

11.vol. 0002www.iiste.org call for paper no. 2_c reinig & ca tilt _pp176-197

- 1. Issues in Social and Environmental Accounting Vol. 2, No. 2 Dec 2008/Jan 2009 Pp. 176-197 Corporate Social Responsibility Issues in Media Releases: A Stakeholder Analysis of Australian Banks Christopher J. Reinig Carol A. Tilt Flinders Business School Flinders University Abstract This paper investigates Australia's four major national banks, analysing the use of media re- leases in the marketing and communication of corporate social responsibility (CSR). Using content analysis, the extent and nature of the media releases issued in 2006, and aimed at spe- cific stakeholders, is determined for each bank. The findings indicate that over one-third of the banks' media releases discuss CSR, predominantly communicating issues related to community involvement. Furthermore, customers and communities are found to be the intended audiences for the majority of the CSR-related media releases. Keywords: CSR, media, banks, Australia, stakeholders, content analysis Introduction sector in the early 1980's, the profits of Australian banks have risen substan- Society is becoming more interested in tially. However, there has also been a the social responsibility of organisations call for increased competitiveness as a (Dawkins & Lewis, 2003; Bartlett, result of deregulation, which has had 2005), who in turn are more aware of dramatic effects on society, such as con- their own actions, fuelled by anti-trust siderable employee downsizing (Bartlett, laws, consumer-protection laws, and 2005). Consequently, there has been in- requirements-to-serve laws (Farmer & tense media and public scrutiny focused Hogue, 1973). Organisations' communi- on the banking industry. Although cation of their corporate social responsi- many studies have considered CSR and bility (CSR) has received close scrutiny social reporting by banks (Enquist, from the media and activist groups, par- 2006; Schneider, 1982; Bank Marketing ticularly in the banking sector. International, 2005; Do et al., 2007) most consider it as a means of respond- Since the deregulation of the banking ing to criticism, rather than as part of a strategy to proactively communicate to Corresponding author: Carol A Tilt, Professor of Accounting & Associate Dean (Research), Flinders Business School, Flinders University, Adelaide, South Australia, Email: Carol.Tilt@flinders.edu.au

- 2. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 177 stakeholders. This paper investigates spective provided by stakeholder theory CSR reporting in the Australian banking is considered to be most appropriate. sector, in particular, the four major na- Thus, a review of stakeholder theory is tional banks are considered: Australia presented below and this section con- and New Zealand Banking Group cludes with a discussion of the strategic (ANZ), Commonwealth Bank of Austra- nature of CSR, how it is used in market- lia (CBA), National Australia Bank ing to communicate with an organisa- (NAB) and Westpac Banking Corpora- tion's stakeholders, and its relevance to tion (WBC). stakeholder theory. The aim of this paper is to identify to what extent Australia's four major na- Stakeholder Management tional banks use their CSR for marketing purposes aimed at specific stakeholders, Stakeholder theory has received much in the context of stakeholder manage- research attention regarding the inclu- ment. The extent and nature of CSR, sion or exclusion of groups or ideas marketed via media releases, by each of (Alkhafaji, 1989; Phillips & Reichart, the banks over the period 1 January to 2000; Radin, 1999). The theory suggests 31 December 2006, is identified. The that organisations must manage their intended audience of each media release various stakeholders individually given is also determined, and the banks’ mar- their expectations of an organisation keting of their CSR examined in light of (Freeman, 1984). Therefore, organisa- stakeholder theory. tions operate not only in consideration of shareholders as argued by Friedman This paper is organised as follows: The (1970), but also in consideration of other next sections outline the theoretical per- stakeholders such as employees, custom- spective that informs this study, and re- ers and communities (Hodgetts, 1996). views the research that has considered Shareholders supporting long-term as stakeholder theory and CSR particularly well as short-term profits cause organi- in a marketing context. Next, the re- sations to build lasting relationships with search methods are described, followed stakeholders, without whose support the by the findings. The subsequent section organisation would cease to exist. An- compares and contrasts the findings with soff (1965) maintains that organisations the views prescribed by stakeholder the- must determine the often-conflicting ory. Finally, conclusions and implica- needs of its stakeholders, and manage tions are presented. them in a way to satisfy as many as pos- sible, or at least the most powerful stake- holders. As noted by Farmer & Hogue Theoretical Framework (1973), given the limited resources any one organisation has, this strategy of An organisation must consider the im- stakeholder management may often re- pact of its operations on its various sult in a trade-off between satisfying stakeholders (Freeman, 1984). As this stakeholders. Thus the need for effective paper examines Australia's four major communication strategies is evident, in national banks' marketing of their CSR order to meet the many demands of to various groups, the theoretical per- stakeholders (Gray et al. 1996).

- 3. 178 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 Deegan (2006) notes however, that the accomplished by assessing three vari- term stakeholder theory is used in differ- ables: power (the extent a party can im- ent contexts. Hasnas (1998, p. 26) states pose its will in a relationship); legiti- that “it is used to refer to both an empiri- macy (socially accepted and expected cal theory of management and a norma- structures or behaviours); and urgency tive theory of business ethics, often (time sensitivity or criticality of the without clearly distinguishing between stakeholder's claims) (Mitchell et al. the two. This study does not consider the 1997). This study attempts to identify normative (ethical) branch of stake- those stakeholders Australia's four major holder theory, which concerns how man- national banks deem influential regard- agers should deal with corporate stake- ing the marketing of their CSR via me- holders (Berman et al. 1999). Rather, it dia releases in the year 2006. examines the positive (managerial) branch of stakeholder theory (Berman et Freeman (1984), defines stakeholder al. 1999) which involves identifying management as the need for an organisa- stakeholders of the organisation and tion to manage the relationships with its managing them in a way that furthers the specific stakeholders in an action- organisation's objectives. Fulop & Lin- oriented way. Organisations face a chal- stead (1999) explain that a major com- lenge to satisfy its stakeholders, depend- plication involved with each strategy ent on both the size of the organisation pursued by an organisation is the task of (with a small organisation, the expecta- fulfilling the best interests of all stake- tions of its stakeholders may not be as holders. As Gray et al. (1996) point out high as with a larger organisation), and however the more important the stake- the returns of the organisation (with holder to the organisation, the more ef- above-average returns, an organisation fort will be exerted by the organisation may find it easier to satisfy stakeholders in managing the relationship. The level than when enjoying average or below- of power a stakeholder has is in part de- average returns) (Hanson & Dowling, termined by the amount of resources 2002). This study assumes the commu- controlled/owned by the stakeholder, as nication of CSR activities via media re- Wallace (1995, p. 87) points out “the leases to be a method of stakeholder higher the group in the stakeholder hier- management. archy, the more clout they have and the more complex their requirements will be”. Literature Review Stakeholder Management: The Busi- A major component of stakeholder the- ness Case ory considers the ability of managers to identify their stakeholders and criticality Freeman (1984, p25) defines stake- to the organisation, allowing effective holders as “any group or individual who stakeholder management to follow. Sev- can affect or is affected by the achieve- eral authors (Mitchell et al. 1997; Han- ment of the organisation's objectives” son & Dowling, 2002) have developed Examples of stakeholders include sup- methods to achieve stakeholder identifi- pliers, customers, employees, sharehold- cation. In particular, it is claimed that ers, and the local community. It has been distinguishing between stakeholders is pointed out, however, that the broadness

- 4. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 179 of Freeman's (1984) definition could point of view, integrating CSR issues lead to the inclusion of competitors or into the discussion where possible. terrorists as stakeholders of an organisa- Deegan et al. (2000) writes: tion (Alkhafaji, 1989, p36). Therefore, Institutions that incorporate stake- Alkhafaji (1989) suggests that stake- holder expectations and commu- holders should only include those groups nity attitudes in their strategic or individuals that have a vested interest planning are likely better posi- in the survival of an organisation. tioned to address business risks and to take advantage of business Maignan & Ferrell (2001) supports the opportunities as they arise. hypothesis that distinct stakeholder groups perceive activities of an organi- Starik (1991) for example, examines the sation differently, therefore requiring relationship between an organisation's tailored marketing efforts aimed at spe- stakeholder management and their repu- cific stakeholders. This conclusion is tation. Using Freeman's (1984) method- drawn after examining and comparing ology to determine the level of stake- the views of internal employees and ex- holder management existent within an ternal customers regarding the activities organisation, and responses from stake- of a French business. holders to gauge reputation status, a positive relationship is found between Similarly, Whysall (2000) highlights the the two variables. Although only focus- importance of stakeholder management ing on consumer-related stakeholder by focusing on the 'mismanagement' of groups for American inventory-owned stakeholders. Using real-life examples electric organisations, the results of this from organisations such as Hoover Co. study still have implications for the and British Gas, the problems discussed reputation of other organisations adopt- regarding specific stakeholders empha- ing similar stakeholder management sise a need for effective stakeholder strategies. Similarly, arguments have management. A major assertion of the been made in favour of an organisation's study is the interaction of stakeholder consideration of the environment im- groups, as opposed to their isolation proving their reputation (Dechant et al. from each other, attributable to the abil- 1994; Hart, 1995). ity of an individual or group belonging to more than one stakeholder group The majority of the literature on the ef- (Cooper, 2003). Hence the mismanage- fects of stakeholder management on or- ment of one stakeholder can potentially ganisations relates to improvements in have widespread effects, therefore by financial performance, as evidenced by outlining how the ineffective strategies the following studies. Berman et al. can cause problems for an organisation, (1999) examined five specific stake- the importance of stakeholder manage- holder issues (employees, product ment is further supported. safety, workplace diversity, communi- ties, and the environment) with positive In assessing the relevant literature sur- results (that is, financial benefits for the rounding the concept of stakeholders, it organisation when adopting stakeholder is necessary to discuss the benefits of management strategies). Employees as such a strategy from an organisation's stakeholders are regarded as a valuable

- 5. 180 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 source of competitive advantage organisation to which the strategy origi- (Berman et al. 1999). Similarly, nates. Their study found that higher lev- Huselid's (1995) study of a cross-section els of stakeholder management may of organisations examined the effects of have a negative impact on CEO salaries. human resource management policies That is, the salaries, bonuses, and com- and practices (aimed at employees) on pensation all decrease with higher levels financial performance. The financial of stakeholder management. Mostly, benefits associated with the effective however, the empirical research re- management of this stakeholder group, viewed is supportive of a stakeholder possibly more straightforward than oth- management strategy from a business ers, are attributed to lower turnover, case perspective. lower absenteeism, and improved pro- ductivity (Huselid, 1995). CSR and the Banking Industry Affecting multiple stakeholder groups, in particular employees and customers, Specific to the banking sector of the fi- is the level of diversity an organisation nancial services industry, Stablein's employs in their workforce (Berman et (1986) study details a case in favour of al. 1999). Visible efforts to recruit and organisations adopting CSR strategies. retain the best people regardless of race, This is attributed to the need for an im- ethnicity, or gender, may improve an proved reputation in the sector, damaged organisation's ability to relate to a broad by fierce competition as a result of de- customer base (Thomas & Ely, 1996), regulation (and although Stablein's and reduce employee turnover or absen- (1986) study originates from the U.S.A., teeism resulting from disgruntled em- similar deregulation in the Australian ployees (Hart, 1995). Integrating CSR banking sector enables comparisons to into a stakeholder management strategy, be made). Robinson & Dechant (1997) explain the general tendency of management to ex- Peterson & Hermans (2004) present a hibit reluctance in their training and de- longitudinal study on the CSR issues velopment of women and minorities. prevalent in the marketing of U.S. banks, using content analysis to examine Although product safety may not appear television commercials. Conducted to to be a CSR issue relevant to this study determine the range of stakeholders at of banks, when adapted to the financial whom the marketing is aimed, the study services industry it can represent secu- also seeks to determine if the increase in rity, such as for ATMs or Internet bank- public awareness of CSR issues results ing. When appropriate strategies are im- in an increase in CSR marketed by the plemented considering the wellbeing of banks. Consequently, resulting from this customers, increased sales are the likely research is the apparent increase in CSR result (Waddock & Graves, 1997). communicated to stakeholders via televi- sion commercials. Taking a different approach, a study by Coombs & Gilley (2005) examine the Margret & Tran (2007) examine attrib- relationship between stakeholder man- utes of corporate social reporting in Aus- agement and salaries of CEOs from the tralia's four major national banks as a

- 6. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 181 reaction to new legislation. Accordingly, share prices yields positive results banks are required to disclose their envi- (although their study is not about CSR). ronmental, social and ethical standards In recognition of a change in public atti- in investment decisions. However, the tudes, managers are required to evaluate results discover no increase in CSR how to communicate their actions for a within the banks, therefore the legisla- range of stakeholders. It has been shown tion has no impact on the level of CSR that the public is generally accepting of engaged in by the banks. In this study, an organisation's communication of their the proactive communication of CSR via CSR for marketing purposes (i.e. to en- media releases is considered rather than hance profitability) (Dawkins & Lewis, CSR as a result of forcible legislation. 2003). However, this still needs to be communicated in an effective manner so Bartlett (2005) adopted a perspective as not to explicitly contradict the similar to most literature reviewed, 'charitable' view of CSR. As detailed by whereby legitimacy theory is considered Swift (2001), due to an increase in social in the research of CSR. Again, CSR re- and ethical auditing, a rise in the com- porting is analysed as a response to me- munication of CSR is evident in organ- dia coverage, rather than as a proactive isational documents (such as media re- communication strategy. The study leases). Such is the case with Belgium shows that the organisations comprising bank KBC which, in accordance with a the Australian banking sector respond to growth in importance of CSR particu- similar concerns in different ways, ulti- larly in the financial services industry, mately affecting reputation rankings of recognised the need to demonstrate its the individual organisations. Therefore CSR achievements (Bank Marketing the implications of Bartlett's (2005) International, 2005). study for this paper is the suggestion that each of Australia's four major national Research on the communication of CSR banks communicate CSR at different appears to be conducted primarily in levels, on different issues. reaction to events that brought the indus- try or organisation into the public spot- light (Deegan et al. 2000). One such Communication of CSR to Stake- study on Australia's four major national holders banks looks at the relationship between the organisations' CSR reporting as a Daniels & Spiker (1991) encourage or- response to legitimacy concerns, and ganisations to focus on stakeholders in their reputations (Bartlett, 2005). Irwin their communication strategies. Among & More's (1994) research looks at the other factors, this is particularly the case possibility of stakeholders to be affected in the area of establishing a desirable by communication intended for another organisational image in the public mind group. In particular, with an organisa- (Daniels & Spiker, 1991). Higgins & tion's communication of CSR to employ- Bannister (1992) show the financial ees conducted internally, external com- benefits associated with communication munication (such as that found in media strategies. In their study, analysing both releases) is thought to have a potentially the level of communication that organi- minor impact on employees. sations aim at stakeholders and relative

- 7. 182 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 Whysall (2005) considers media re- gate Australia's four major national leases. Specifically, the study seeks to banks' communication of their CSR in increase understanding on the role, con- light of stakeholder theory. Media re- tent and effectiveness of supermarkets' leases are a major source of information media releases. Whysall (2005) finds aimed at stakeholders, being a popular that media releases generally attract lim- feature of organisations' Websites ited attention from the audiences tar- (Cooper, 2003). Despite the importance geted. Furthermore, examination of me- placed on the Internet as a communica- dia releases from supermarkets leads to tion tool, research indicates that the the conclusion that there is a need to number of studies considering this is research the content and function of me- limited (Tomasello, 2001). The majority dia releases in sectors where stakeholder of studies considering stakeholder man- relations are important. agement via communication strategies do not consider media releases. Rather, Finally, Cooper's (2003) study centres as with Bartlett's (2005) study, analysis on the Internet as the medium used for of annual reports, social impact reports communicating with stakeholders. Coo- and policy statements predominates. per (2003) highlights the potential for an individual or group to have multiple "stakes" in an organisation given the Sample Selection results of the analysis. This conclusion is achieved by examining the relationships The sample comprises the four major formed between various stakeholder national banks in Australia for the year groups and the organisations. It is dis- 2006. The financial services industry is covered that employees and managers regularly under criticism regarding CSR. receive less attention via the Internet due This focus of attention on the industry to the tendency of organisations' manag- could be attributed to the ability of the ers and marketers to communicate to organisations comprising this industry to their employees via internal means. affect the operational activities and out- Similarly, customers do not receive sig- comes of a variety of organisations nificant attention due to the structure of across diverse industries (Margret & the electricity industry, with many or- Tran, 2007). Supporting the purposive ganisations in this industry not dealing selection of Australia's four major banks directly with end-customers. as the sample for consideration in this study, Farmer & Hogue (1973, p. 5) re- This study considers media releases as a port on the expectations of society to- form of communication of CSR issues wards large organisations: and attempts to link them to particular Most people do not expect smaller stakeholder groups. The method for this firms to do much toward carrying analysis is presented next. costs of anti-pollution campaigns, to contribute heavily to educa- tional funds, or to lead businesses Research Method in working toward similar socially desirable goals. This is an exploratory case study in which media releases are used to investi- Therefore the choice of selecting sample

- 8. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 183 for analysis is attributable to both the content analysis can be used to: relevance of CSR to the financial ser- • identify the intentions of the commu- vices industry and the higher expecta- nicator tions from society towards CSR in these • describe trends in communication larger organisations. A limitation of this content non-probability sampling design, how- • reveal the focus of individual, group, ever, is the inability of the results to be institutional, or societal attention generalised to a population (Cavana et al. 2001). Content analysis has been described as: A technique for gathering data Every media release for the year 2006 that consists of codifying qualita- was obtained through each bank's Inter- tive information in anecdotal and net site. There were 79 media releases literary form into categories in from ANZ; 99 media releases from order to derive quantitative scales CBA; 48 media releases from NAB, of varying levels of complexity and; 89 media releases from WBC (a (Abbott & Monsen, 1979 p504). total of 315) for the period of analysis. Only ANZ's Website has a separate link Consistent with this description, content for media releases solely on CSR-related analysis is useful for identifying themes issues. Of the 28 media releases in in the raw data (Cavana et al. 2001). ANZ’s link specifically for their CSR- With the objective of determining the related media releases, 26 are considered existence of stakeholder management in this study as two were not accessible via media releases, each media release due to a broken link. was read and classified into one of the identified themes (see below). The re- All media releases were considered and lease was then read in detail to deter- judged according to the coding rules (see mine the stakeholders at whom the me- below). That is, each media release is dia release is aimed. This classification analysed to determine if it discusses any method is, like most content analysis, of the CSR issues listed in Table 1, and quite subjective, therefore, specific cod- the stakeholder at whom these media ing rules were prepared for analysis of releases are aimed was determined. the media releases, including definitions Every media release was thoroughly as- for each theme, treatment of multiple sessed to determine if it discussed more themes, treatment of headings, etc. A than one CSR issue, or if it was aimed at sample of releases was then re-coded by more than one stakeholder. a second coder and the results reviewed. The specific CSR themes used were Coding and Analysis adapted from existing literature. Hodgetts & Kuratko's (1991) study lists In order to measure the extent and nature general CSR issues that organisations of CSR in the media releases, content must deal with in contemporary society. analysis is used. Weber (1985) points The themes used are presented in Table out several purposes of content analysis, 1. The coding sheet and rules are derived all dependent on the objectives of the from Riffe et al. (2005). Multi-case cod- research. Relevant to this study is that ing sheets were used for the analysis, as

- 9. 184 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 these are useful when there are a large Communities; and Other. These are the number of cases (in this study, the cases most commonly identified stakeholders are the individual media releases) (Riffe for CSR disclosure (Estes, 1976; Ogan et al., 2005). The stakeholders as identi- & Ziebart, 1991; Tilt, 1997; 2007), but fied by Donaldson & Lorsch (1983) are the ‘other’ category was included to adapted for use in this study and include identify any stakeholders specific to the Shareholders; Employees; Customers; organisations under study. Table 1 CSR Themes Used in Analysis Environment: pollution control; restoration or protection of environment; Energy: conservation of energy in production and marketing operations; Fair Business Practices: employment and advancement of women and minorities; support for minority owned business; Human Resources: employee training and development; Community Involvement: donations of cash, products, services or employee time; sponsorship of public health projects; support of education and the arts; support of community recreation programs; cooperation in community projects; Products: enhancement of security; environmental/ social improvements of a product. overlapping nature is another limitation. As an example of how media releases This study however, is exploratory in were coded, the release entitled nature as the area of CSR marketing to ‘Commonwealth Bank activates emer- stakeholders has not been researched gency package to help cyclone vic- previously to any great extent. tims’ (Commonwealth Bank of Austra- lia, 20th March 2006) totaled 282 words. On reading this example it was assigned Results various codes in the coding sheet CSR Themes in Media Releases (spreadsheet) as it was identified as be- ing CSR-related, then coded for The media releases from Australia's four 'community involvement (donations of major national banks are slightly differ- cash, products, services or employee ent in their presentation on the websites. time), and for each stakeholder men- Australia and New Zealand Banking tioned in the report directly (customers Group’s (ANZ) site has two separate and local farmers). links for their media releases in 2006: one titled 'ANZ 2006 Media Releases' Some media releases did not mention a and one titled 'ANZ 2006 Corporate Re- stakeholder directly, and in these cases sponsibility Media Releases'. The other they were read in their entirety and a banks do not distinguish between CSR- subjective decision made as to which related and non-CSR-related media re- stakeholders, if any, were the intended leases. National Australia Bank’s (NAB) audience. Such subjectivity is inherent in site for its media releases in 2006 is ti- content analysis, and is acknowledged as tled 'Media Releases/ASX Announce- a limitation. Similarly, stakeholder cate- ments', incorporating information on the gories are not entirely discrete, so their Australian Stock Exchange aimed at

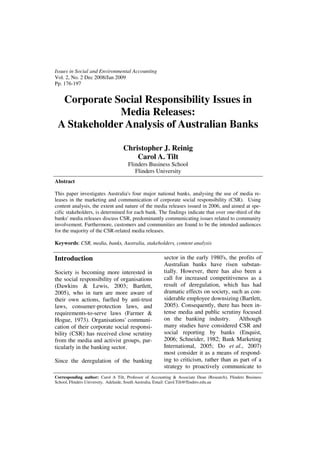

- 10. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 185 both current and potential investors. municate one CSR theme (23 media re- Westpac Banking Corporation (WBC) leases are found to discuss two CSR is- and Commonwealth Bank of Australia sues). This conclusion is supported by (CBA) both title the link for their media the tendency for all banks to occasion- releases in 2006 simply 'Media Re- ally publish several media releases per leases'. day. Figure 1 shows the number of me- dia releases issued by each bank in 2006, The ease associated with accessing the and the corresponding number of media media releases is interesting given an releases involving CSR. 117 media re- aim of this study is to determine the leases out of a total of 315 discuss CSR level of attention given to different (approximately 37%) highlighting the stakeholders. On the homepage of ANZ, significance of CSR in the banking sec- CBA, or WBC, media releases are found tor of the financial services industry. by clicking on either the 'about us', 'glossary', or 'info' links, respectively. Figure 1 shows that NAB does not com- This presents a link to the 'Media Cen- municate via media releases as much as tre', which exists in all four bank web- the other banks, with only 48 releases, sites. NAB is the only bank for which but their CSR-related media releases the Media Centre is accessible directly amounted to 41% of these, the second from the Homepage. However, all of the highest proportion. The type and banks' Websites feature a 'Search' func- amount of CSR discussed in the media tion accessible from any of their Web- releases, is presented for each of the sites. The usability of websites is an in- banks in Table 2, noting that 23 media teresting area for future research; see releases communicate more than 1 CSR Tilt et al. (2008). theme, resulting in a higher number of CSR issues discussed than the total num- It is evident that CSR is a significant ber of CSR-related media releases. Each issue reported upon in the media releases sub-category is considered in detail in of Australia's four major national banks. the following sections. The majority of the media releases com- N umbe r o f M e dia R e le a s e s Fo cus ing o n C S R 120 99 89 100 # of Media Releases 79 80 48 T ota l 60 C S R -R e la te d 40 20 34 33 20 30 0 AN Z C BA N AB W BC Ban k s Figure 1 Number of Media Releases Focusing on CSR

- 11. 186 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 Table 2 Type and Amount of CSR in Media Releases ANZ CBA NAB WBC Total Environment 2 - - 4 6 Energy 1 - - 1 2 Fair Business Practices 2 1 1 3 7 Human Resources 2 1 - 1 4 Community Involvement 33 32 18 22 105 Products 4 4 4 6 18 Total 44 38 23 37 142 Community Involvement this issue in their media releases more Table 2 shows that media releases focus- often than they discuss donations. ing on community involvement are the most common. Community-related is- Energy sues are discussed in the media releases Table 2 shows that only two media re- approximately 74% of the time in rela- leases communicate an energy-related tion to total CSR themes. The majority issue for the year 2006 (less than 2% of of these community-related media re- the attention in relation to the other CSR leases involve donations of cash, prod- themes). For example, ANZ's energy- ucts, services, or employee time. The related media release titled 'ANZ devel- most popular form of community in- ops Australia's largest office building in volvement concerns assistance to those Melbourne' (Australia and New Zealand affected by a natural disaster, however, Banking Group, 27th September 2006), WBC appears to aim these media re- discusses the various energy-efficient leases solely to its customers, never dis- measures incorporated into ANZ's new- cussing any initiatives involving the do- est office building. It is now worth not- nation of cash to communities affected ing that ANZ's media releases are found by a natural disaster. This could be be- to communicate the widest range of is- cause they did not donate to those com- sues to its stakeholders, regarding CSR. munities indicating that customers are A reason for the lack of energy-related given higher priority. The other banks media releases is possibly the nature of aim these media releases towards both the banking sector. More specifically, customers and communities, often do- the intangibility of banks' products, and nating cash to those that are not neces- the minimal amount of energy required sarily customers. for a bank's operations, allows little op- portunity to implement energy-saving A significant portion of the media re- initiatives. leases focusing on community involve- ment relate to the support of education Environment or the arts, with all banks communicat- Only ANZ and WBC issued CSR- ing this issue in their media releases. related media releases involving the en- Interestingly, CBA is the only bank con- vironment to stakeholders in 2006. CSR sidered in this study that communicates issues relating to the environment are

- 12. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 187 discussed approximately 4% of the time promotion of a product designed to have in relation to the other CSR themes. In a positive environmental or social im- particular, these media releases discuss pact. For example, WBC's media release either a commitment to the restoration or titled 'Westpac enhances Internet Bank- protection of the environment, or pollu- ing security' (Westpac Banking Corpora- tion control. For example, WBC (being tion, 13th February 2006) discusses en- the bank using media releases to com- hanced security provided for online municate environmental issues to its banking. stakeholders more than any other of Australia's major national banks), in the media release titled 'Westpac extends Stakeholder Analysis of Media Re- highly successful paper saving initia- leases tive' (Westpac Banking Corporation, 8th August 2006), discusses the extension of It is evident that each of Australia's four their e-statement strategy aimed at sav- major national banks tailors its media ing paper. Again, issues involving the efforts, at least regarding CSR, to each environment may not be communicated of its stakeholders. Furthermore, the re- to a great extent in media releases given sults indicate that the banks focus on the tendency of the banks to use other similar issues, highlighting a trend in the means, such as environmental reports. banking sector. Fair Business Practices and Human As discussed earlier, Freeman (1984) Resources describes stakeholder management as Table 2 shows that media releases in- the need for an organisation to manage volving the banks' fair business practices the relationships with its specific stake- and human resources (HR) are rare - holders in an action-oriented way. An approximately 5% in relation to the objective of this study is to determine other CSR themes for Fair Business and those stakeholders at whom the CSR- 3% for HR. A possible reason for the related media releases from Australia's lack of media releases in these areas is four major national banks are aimed. that they are aimed at employees and Figure 2 (see the next page) shows the organisations may use other means to stakeholders considered by Australia's communicate to its employees (for ex- four major national banks and the num- ample an Intranet or staff notice board). ber of media releases aimed at each. Products Just as there are 23 media releases com- Out of all media releases products re- municating more than one CSR theme to lated to CSR are given approximately stakeholders, there are 25 media releases 12% of the attention in relation to the aimed at more than one stakeholder other CSR themes, and exist for all of group, resulting in totals greater than the banks. Given the nature of the bank- 100%. Table 3 shows the percentage of ing sector, improvements in services media releases aimed at each stake- such as Internet banking, and security holder group by theme. For example, upgrades at ATMs, are included in this 100% of the media releases discussing section. Specifically, these media re- fair business practices are aimed at cus- leases discuss the introduction or the tomers, 42.9% of these media releases

- 13. 188 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 Stakeholders Targeted in Media Releases 90 83 80 73 70 # CSR Media Releases 60 50 40 30 20 13 7 10 0 0 Shareholders Emp loy ees Customers Communities Other Stakeholders Figure 2 Stakeholders Targeted in CSR Media Releases Table 3 Percentage of Media Releases Aimed at Stakeholders by Theme Shareholders Employees Customers Communities Environment - 16.7% 100% 33.3% Energy 50% 50% 50% 50% Fair Business Practices - 42.9% 100% 42.9% Human Resources 25% 100% 75% 50% Community Involvement 2.7% 3.8% 46.7% 59% Products 11.1% - 94.4% 16.7% are aimed at employees, and 42.9% of releases detailing the efforts of an or- these media releases are aimed at com- ganisation to reduce waste (or some munities. other cost-saving method) appear to sup- port this. For example, the media release Shareholders from WBC titled 'Westpac extends Figure 2 shows that shareholders are one highly successful paper saving initia- of the stakeholder groups considered in tive' (Westpac Banking Corporation, 8th the CSR-related media releases from August 2006) details a CSR initiative Australia's four major national banks in resulting in cost savings. 2006, albeit rarely. Cooper (2003) con- cludes that the majority of environment- Although it is traditionally thought that related communication is aimed at shareholders are an organisation's most shareholders and in this study media important stakeholder group, the results

- 14. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 189 from this study conclude that, regarding potential future employees. This sup- the communication of CSR via media ports the research finding that employ- releases shareholders are not considered ees would prefer to work for an organi- the most important stakeholder group. sation promoting their growth, or at least This supports Dawkins & Lewis (2003) would be less likely to leave the com- who also show that the importance of pany (Huselid, 1995). Dawkins & CSR to the investment community Lewis (2003) argue that it is in the best (shareholders) is lower than other stake- interests of an organisation to communi- holder groups. cate their CSR towards its employees, given the importance of employee advo- Employees cacy on other stakeholders. Although the Huselid (1995) examined the effects of results of this study suggest Australia's human resource management policies four major national banks do not do this and practices on financial performance. via media releases, but rather use inter- The financial benefits associated with nal methods to communicate with them the effective management of this stake- (such as an Intranet or staff notice holder group, possibly more straightfor- boards). ward than others, are attributed to lower turnover, lower absenteeism, and im- Customers proved productivity (Huselid, 1995). Customers are a major focus of Austra- Therefore research informs us that it is lia's four major national banks’ media in the best interests of an organisation to releases. One CSR issue discussed by all not only engage in workplace diversity, the banks in their media releases is the but to communicate this to employees. enhancement of security, such as at ATMs and Internet banking. These CSR Specific to this study, media releases issues are aimed at both current and po- discussing the advancement of women tential customers. Clearly, customers or minorities are issues and are aimed at prefer to ensure their wealth is kept as both current and potential employees. secure as possible. It is again appropriate Furthermore, the level of diversity an to point out the potential for a person or organisation employs in their workforce group to have multiple "stakes" in an is also found in the releases, and is organisation (Cooper, 2003), however in aimed at employees (Berman et al. a different manner. For example, it is 1999). As discussed earlier, an organisa- logical to assume that a considerable tion's visible efforts to recruit and retain number of an organisation's employees people regardless of race, ethnicity, or are also customers. To eliminate confu- gender, may reduce employee turnover sion, this sub-section only considers or absenteeism resulting from disgrun- those stakeholders as customers, regard- tled employees (Hart, 1995). Therefore less of the other stakeholder groups to marketing these CSR issues to employ- whom they belong. ees is intended to have a positive impact on the organisation and its employees. Furthermore, incorporating environ- mental aspects in a product is often Similarly, media releases discussing em- aimed at customers. This is understand- ployee training or development are able given the growing trend for custom- aimed at both current employees and ers to consider the environmental impact

- 15. 190 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 of their purchasing (Dawkins & Lewis, own reputation when marketed in con- 2003). Therefore research supports the junction with a well-known event or idea that those organisations marketing cause (Dechant et al. 1994; Hart, 1995). products that have a positive impact on Therefore, shareholders supporting long- the environment are more likely to at- term as well as short-term profits are tract new customers and retain existing supportive of investments in community customers. It is thus in the best interests issues such as sporting events, positively of Australia's four major national banks affecting their own long-term wealth to create environmentally friendly prod- (Donaldson & Lorsch, 1983). ucts and market them towards custom- ers. Gray et al. (1996) point out that the more important the stakeholder to the The finding that customers are given the organisation, the more effort will be ex- most attention regarding the banks' mar- erted by the organisation in managing keting of CSR via media releases in the the relationship. Given the results of this year 2006 has implications stemming study it would appear that, regarding the from the work of Mitchell et al. (1997). communication of CSR via media re- To recall, their study details a method leases, communities are considered one for stakeholder identification, in particu- of the most important stakeholders. This lar the ability to distinguish between is true for each of Australia's four major stakeholders by assessing three vari- national banks, each focusing their CSR- ables: power; legitimacy; and urgency. related releases to communities (and Given the results of this study, it is evi- customers). A reason presented in a dent that, relative to shareholders and study by Waddock & Graves (1997) that employees, customers are critical re- supports an organisation's improvement garding the marketing of CSR via media of community relations is the potential releases in the year 2006. The trend for savings experienced in the form of tax all banks to aim the majority of their advantages. marketing of CSR towards customers reinforces this assertion. Given the extent to which communities and customers are focused on in the Communities banks' CSR-related media releases rela- Communities are the intended audience tive to other stakeholders, it could be of the banks' media releases almost as thought that these two stakeholder much as customers. A reason for Austra- groups drive the CSR strategies adopted lia's banks to aim their CSR-related me- by the banks. That is, CSR initiatives are dia releases at communities is the wide stakeholder-driven rather than simply range of people that may be included in marketed to suit the current strategies. this stakeholder group. For example, This finding not only has important im- customers may find themselves affected plications for the marketing strategies of by a community issue supported by an the banks, but also for stakeholders. The organisation. Furthermore, by being at- extent to which a stakeholder group can tached to a well-known event or cause, impose its will in a relationship with an organisations in turn gain their own pub- organisation may influence the strategies licity. More specifically, organisations adopted by that organisation. experience a positive impact on their

- 16. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 191 Discussion and Conclusions CSR-related media releases, consistent with stakeholder management. By aim- Despite the abundance of literature ing them at specific stakeholders, the available on CSR in marketing and CSR banks successfully differentiate between reporting, few studies consider an or- their intended audiences. ganisation's use of media releases to communicate to stakeholders. This paper According to stakeholder theory organi- presents a case study on the Australian sations will attempt to balance the com- banking sector, examining the media peting and often conflicting interests of releases from 2006 from Australia's four its stakeholders. The findings of this major national banks, to determine the study reveal that shareholders and em- extent and nature of CSR aimed at spe- ployees receive some attention, however cific stakeholders. The study found a it is customers and communities at trend in both the CSR issues communi- whom most of the CSR-related media cated via media releases from each of releases are aimed. By determining the Australia's four major national banks extent of CSR aimed at specific stake- and the level of attention given to each holders, this study aims to highlight an stakeholder group. The media releases organisation's recognition of the growing focus primarily on community involve- importance of social and environmental ment relative to the other CSR themes issues in contemporary society. For the and are aimed primarily towards cus- Australian national banking sector, over tomers and communities. one-third of all media releases from the year 2006 discuss CSR. Furthermore, Friedman (1970) argues that CSR takes the banks' media releases discuss com- away from the profits of shareholders, munity initiatives as they relate to CSR with increases in share-price being an considerably more than any other CSR organisation's sole responsibility. In re- issue. cent times however, the responsibilities The organisational strategy of stake- of organisations have extended relative holder management, consistent with to the impact of their operations on soci- views prescribed by stakeholder theory, ety. Accordingly, stakeholder theory asserts that organisations must determine prescribes that an organisation must con- the needs of their various stakeholders sider a wide range of interests to achieve and attempt to satisfy the claims of those its own objectives and ensure the sur- most powerful. Reasons for possible vival of the organisation (Freeman, trends in the data are proposed in light of 1984). It is thought that the managerial stakeholder theory: (1) given the con- (positive) branch of stakeholder theory flicting views of profit-maximisation is most relevant to this study, given it and CSR organisations may be less seeks to examine Australia's four major likely to market their CSR initiatives to national banks' communication of their shareholders; (2) employees are found to CSR to various groups. This is consis- rarely be the target for the banks' CSR tent with the view that CSR serves a marketing, possibly due to the tendency wider community (Freeman, 1984). The for organisations to use internal means results of this study suggest that Austra- to communicate to this stakeholder lia's four major national banks consider a group; (3), the satisfaction of customers wide range of interests in their use of is important in any organisation, and the

- 17. 192 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 satisfaction of this stakeholder group is Limitations important for increased sales; (4) the amount of attention given to communi- No methodology existed prior to this ties as a stakeholder group in the CSR- study for determining the stakeholders related media releases is attributed to the being targeted by corporate communica- wide range of stakeholders potentially tions. Therefore, a subjective approach affected by such communication. using content analysis was applied. Fur- thermore, media releases are analysed as a means of communicating CSR to Implications stakeholders, excluding other means such as television, radio, and annual re- The results of this study suggest that ports. As these are also popular sources stakeholder management is a strategy of advertising, this study may not com- adopted by the banks regarding the com- prehensively represent the marketing munication of CSR via media releases. efforts of the banks. The implementation of effective com- munication strategies is important when considered in light of results from the Further research research of Dawkins & Lewis (2003), suggesting only 36% of people are able Similar to the study by Peterson & Her- to recall any examples of an organisation mans (2004) this study could be con- helping society or the community, there- ducted in a longitudinal form to see if fore the results of this study have impli- there has been a significant change in cations for our understanding of the use the marketing of CSR relative to of CSR in a marketing context changes in societal attitudes. This would provide insight into possible changing The findings indicate community in- stakeholder attitudes and associated or- volvement is communicated to stake- ganisational strategies. Furthermore, holders considerably more than any Schneider (1982) outlines the potential other CSR theme and customers and benefits arising from measuring one's communities are the target of most CSR- own performance, specifically when ap- related media releases. All four banks plied to an organisation's CSR. Schnei- appear to use the same strategies how- der (1982) claims banks can benefit by ever, so there is little to differentiate assessing the repercussions of the CSR them. strategies they have implemented. Fur- ther research could analyse the repercus- Emphasising this need for marketing sions of the CSR aimed at specific stake- research, Maignan & Ferrell's (2001) holders in conjunction with the organisa- found stakeholder groups perceive the tion's marketing via print media or other- activities of an organisation differently, wise, to assist in the implementation of therefore requiring tailored marketing effective CSR strategies. Finally, Uner- efforts. The results of this study support man & Bennett (2004) argue that organi- the increase in marketing of CSR aimed sations should respond to the needs of at specific stakeholders, or the marketing those stakeholders with whom they en- of CSR via other media. gage with as opposed to solely those stakeholders owning or controlling re-

- 18. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 193 sources. Thus, further research on the ing Industry”, Proceedings 34th interaction between organisations and European Marketing Academy stakeholders around CSR issues in me- Conference 2005, Milan. dia releases analysed would be enlight- Berman, S. L., Wicks, A. C., Kotha, S. ening. & Jones, T. M., (1999) “Does stakeholder orientation matter? The relationship between stake- References holder management models and firm financial performance”, Abbot, W. F. & Monsen, R. J., (1979) Academy of Management Journal, “On the Measurement of Corpo- Vol. 42, No. 5, pg. 488-505. rate Social Responsibility: Self- Carney, T. F., (1972) Content Analysis: Reported Disclosures as a Method A Technique for Systematic Infer- of Measuring Corporate Social ence from Communications, Lon- Involvement”, Academy of Man- don: University of Manitobba agement Journal, Vol. 22, No. 3, Press. pp. 501-515. Cavana, R. Y., Delahaye, B. H. & Alkhafaji, A. F., (1989) A Stakeholder Sekaran, U., (2001) Applied Busi- Approach to Corporate Govern- ness Research: Qualitative and ance: Managing in a Dynamic Quantitative Methods. Brisbane: Environment, New York: Quorum John Wiley and Sons, Books Commonwealth Bank of Australia, Ansoff, I., (1965) Corporate Strategy, (2007)http://www.commbank. New York: McGraw Hill, Inc. com.au. Australia and New Zealand Banking Commission of European Communities, Group, (2007), http:// (2001) Promoting a European www.anz.com.au. Framework for Corporate Social Argandona, A., (1998) “The Stake- Responsibility, Green Paper, holder Theory & the Common Commission of European Com- Good”, Journal of Business Eth- munities, Brussels. ics, Vol. 17, No. 9, pp. 1093- Coombs, J. E. & Gilley, K. M., (2005) 1102. “Stakeholder management as a Asher, J., (1991) “When a Good Cause predictor of CEO compensation: is also Good Business”, Bank main effects and interactions with Marketing, Vol. 23, No. 6, pp. 30- financial performance”, Strategic 32. Management Journal, Vol. 26, Bank Marketing International, (2005) No. 9, pp. 827-840. KBC Publishes its first CSR re- Cooper, S. M., (2003) “Stakeholder port, London. communication and the Internet in Bank Marketing International, (2006) UK electricity companies”, Banks face CSR Activist Backlash, Managerial Auditing Journal, London. Vol. 18, No. 3, pp. 232-243. Bartlett, J., (2005) “Addressing Con- Corrado, F., (1984) Media For Manag- cerns About Legitimacy: A Case ers. Englewood Cliffs, New Jer- Study of Social Responsibility sey: Prentice-Hall. Reporting in the Australian Bank- Daniels, T. & Spiker, B., (1991) Per-

- 19. 194 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 spectives on Organizational Com- Enquist, B., Johnson, M. & Skalen, P., munication. Dubuque, Iowa: Wm. (2006) “Adoption of Corporate C. Brown. Social Responsibility - Incorporat- Dawkins, J. & Lewis, S., (2003) “CSR ing a Stakeholder Perspective”, in Stakeholder Expectations and Qualitative Research in Account- their Implications for Company ing and Management, Vol. 3, No. Strategy”, Journal of Business 3, pp. 188-207. Ethics, Vol. 44, No. 2-3, pp. 185- Estes, R.W., (1976) Corporate Social 193. Accounting. New York: John Dechant, K., Altman, B., Downing, R. Wiley & Sons. M. & Keeney, T., (1994), Farmer, R. N. & Hogue, W. D., (1973) “Environmental leadership: From Corporate Social Responsibility. compliance to competitive advan- USA: Science Research Associ- tage; Executive commentary”, ates, Inc., . The Academy of Management Ex- Fenn, D., (1995) “The unexpected ad- ecutive, Vol. 8, No. 3, pp. 7-27. vantage”, Inc. Magazine, Vol. 17, Deegan, C., (2006) Financial Account- No. 18, p. 119. ing Theory 2nd ed. New South Freeman, R. E., (1984) Strategic Man- Wales, Australia: McGraw-Hill,. agement: A stakeholder approach. _________, Rankin, M. & Voght, P., Boston: Pitman Publishing. (2000) “Firms’ Disclosure Reac- Friedman, M., 13th September (1970), tions to Major Social Incidents: “The social responsibility of busi- Australian Evidence”, Accounting ness is to increase its profits”, Forum, Vol. 24, No. 1, pp. 101- New York Times Magazine, The 130. New York Times Company. Donaldson, G. & Lorsch, J. W., (1983) Fulop, L. & Linstead, S., (1999) Man- Decision Making at the Top: The agement: A Critical Text. South Shaping of Strategic Direction, Yarra, Australia: MacMillan Busi- New York: Basic Books, pp. 37- ness. 40. Gidengil, B. Z., (1977) “The social re- Donaldson, T. & Preston, L. E., (1995) sponsibilities of business - what “The stakeholder theory of the marketing executives think”, corporations: concepts, evidence European Journal of Marketing, and implications”, The Academy Vol. 11, No. 1, p. 72. of Management Review, Vol. 20, Gray, R., Owen, D. & Adams, C., No. 1, pp. 65-91. (1996) Accounting and Account- Do H, Tilt C. A. & Tilling M.V. (2007) ability: Changes and Challenges “Social and Environmental Re- in Corporate Social and Environ- porting by Westpac Bank”, Pro- mental Reporting. London: Pren- ceedings of the Asia Pacific Inter- tice Hall. disciplinary Research in Account- Grey, A., Kaplan, D. & Lasswell, H. D., ing (APIRA) Conference, Auck- (1965), “Recording and context land, July. (online at: units- four ways of coding edito- http://www.mngt.waikato.ac.nz/ rial content”, in Lasswell, H. D., ConferenceManager/report.asp? Leites, N. and Associates (eds.), issue=5) Language of Politics. Cambridge:

- 20. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 195 MIT Press. sibility: Exploring Stakeholder Hanson, D. & Dowling, P., (2002) Stra- Relationships and Programme tegic Management: Competitive- Reporting across Leading FTSE ness and Globalisation, Victoria, Companies”, Journal of Business Australia: Nelson Thomson Ethics, Vol. 61, No. 1, pp. 7-28. Learning. Kok, P., Wiele, T., McKenna, R. & Hart, S. L., (1995) “A natural-resource- Brown, A., (2001) “A Corporate based view of the firm”, The Social Responsibility Audit Academy of Management Review, Within a Quality Management Vol. 20, No. 4, pp. 986-1014. Framework”, Journal of Business Hasnas, J., (1998) “The normative theo- Ethics, Vol. 31, No. 4, pp. 285- ries of business ethics: a guide for 297. the perplexed”, Business Ethics Kroszner, R. & Strahan, P. E., (2001) Quarterly, Vol. 8, No. 1, pp. 19- “Bankers on boards: monitoring 42. conflicts of interest and lender Higgins, R. & Bannister, B., (1992) liability”, Journal of Financial “How corporate communication Economics, Vol. 62, No. 3, pp. of strategy affects share price”, 415-452. Long Range Planning, Vol. 25, Maignan, I. & Ferrell, O. C., (2001) No. 3, pp. 27-35. “Antecedents and Benefits of Hodgetts, R. M. & Kuratko, D. F., Corporate Citizenship: An Investi- (1991) Management 3rd ed. San gation of French Businesses”, Diego: Harcourt Brace Jovano- Journal of Business Research, vich. Vol. 51, No. 1, pp. 37-51. Hodgetts, R. M., (1996) “A conversa- Margret, J. E. & Tran, B. X., (2007) tion with Warren Bennis on lead- “APIRA 200 Corporate Social ership in the midst of downsiz- Reporting of the Four Major ing”, Organizational Dynamics Banks in Australia from 2002 to Summer edn., pp. 62-78. 2006”, Victoria, Australia. Huselid, M. A., (1995), “The impact of Mathis, A., (2007) “Corporate social human resource management responsibility and policy making: practices on turnover, productiv- what role does communication ity, and corporate financial per- play?”, Business Strategy & the formance”, Academy of Manage- Environment, Vol. 16, No. 5, pp. ment Journal, Vol. 38, No. 3, pp. 366-385. 635-672. Mitchell, R. K., Agle, B. R. & Wood, D. Irwin, H. & More, E., (1994), Managing J., (1997) “Toward a Theory of Corporate Communication. New Stakeholder Identification and South Wales, Australia: Allen & Salience: Defining the Principle Unwin. of Who and What Really Kaler, J., (2003) “ Differentiating stake- Counts”, The Academy of Man- holder theories”, Journal of Busi- agement Review, Vol. 22, No. 4. ness Ethics, Vol. 46, No. 1, pp. 71 pp. 853-866. -83. Mitroff, I., (1983) Stakeholders of the Knox, S., Maklan, S. & French, P., Organizational Mind. San Fran- (2005) “Corporate Social Respon- cisco: Jossey Bass.

- 21. 196 C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 Morgan, D., (2005) “Valuing values at University of Georgia, USA. the heart of the enterprise is how Swift, T. A., (2001) "Trust, Reputation, you create sustainable profit”, The and Corporate Accountability to Age, Australia, August 18th Stakeholders", Business Ethics: A National Australia Bank, (2007), http:// European Review, Vol. 10, No. 1, www.nab.com.au. pp. 16-26. Ogan, P., & Ziebart, D.A., (1991) Thomas, D. A. & Ely, R. J., (1996) "Corporate Reporting and the Ac- “Making differences matter: A counting Profession: An Interpre- new paradigm for managing di- tive Paradigm", Journal of Ac- versity”, Harvard Business Re- counting, Auditing & Finance, view, Vol. 74, No. 5, pp. 79-90. Vol. 6, No. 3, pp. 387-406. Tilt C.A. (1997) “Environmental Poli- Peterson, R. T. & Hermans C. M., cies of Major Companies: Austra- (2004) “The communication of lian Evidence”, British Account- social responsibility by US ing Review, Vol. 29, No. 4, pp. banks”, The International Journal 367-394. of Bank Marketing, Vol. 22, No. _______ (2007) “External Stakeholders’ 3, pp. 199-211. Perspectives on Sustainability Phillips, R. A. & Reichart, J., (2000) Reporting” in Unerman J., O’D- “The Environment as a Stake- wyer B., & Bebbington J. (eds) holder? A Fairness-Based Ap- Sustainability Accounting and proach”, Journal of Business Eth- Accountability, London: Routlege. ics, Vol. 23, No. 2, pp. 185-198. _______, Davidson R.A. & Tilling M.V. Radin, T. J., (1999) Stakeholder Theory (2008) “NGO Communication and the Law, University of Vir- and Activism via Electronic Me- ginia, USA. dia: Australian Evidence”, Third Riffe, D., Lacy, S. & Fico, F. G., (2005) Sector Review, Special Issue, Vol. Analyzing Media Messages: Us- 14, No. 2, pp. 75-96. ing Quantitative Content Analysis Tomasello, T., (2001) “The status of in Research, Lawrence Erlbaum Internet-based research in five Associates, New Jersey, USA. leading communication journals, Robinson, G. & Dechant, K., (1997) 1994-1999”, Journalism & Mass “Building a business case for di- Communication Quarterly, Vol. versity”, The Academy of Man- 78, No. 1, pp. 659-674. agement Executive, Vol. 11, No. Unerman, J. & Bennett, M., (2004) 3, pp. 21-31. “Increased Stakeholder Dialogue Schneider, B. L., (1982) “Corporate So- and the Internet: Towards Greater cial Responsibility: Measuring Corporate Accountability or Rein- Performance - Part II”, United forcing Capitalist Hegemony?”, States Banker, Vol. 93, No. 8, pp. Accounting, Organizations and 38-39. Society, Vol. 29, No. 7, pp. 685- Starik, M., (1991) “Stakeholder man- 707. agement and firm performance: Waddock, S. A. & Graves, S., (1997) Reputation and financial relation- “The corporate social perform- ships to United States electric util- ance-financial performance link”, ity consumer-related strategies”, Strategic Management Journal,

- 22. C.J. Reinig, C.A. Tilt / Issues in Social and Environmental Accounting 2 (2008/2009) 176-197 197 Vol. 18, No. 4, pp. 303-317. -28. Wallace, G., (1995) “Balancing conflict- Whysall, P., (2005) “Retailers’ press ing stakeholder requirements”, release activity: market signals for Journal for Quality and Partici- stakeholder engagement?”, Euro- pation, Vol. 18, No. 2, pp. 84-98. pean Journal of Marketing, Vol. Weber, R. P., (1985) Basic Content 39, No. 9-10, pp. 1118-1132. Analysis, Beverly Hills, USA: Yin, R. K., (1984) Case Study Research: Sage University Paper. Design and Methods. Sage Publi- Westpac Banking Corporation, (2007) cations, USA. http://www.westpac.com.au. Young. J., (1991) “Reducing waste, sav- Whysall, P., (2000) “Stakeholder mis- ing materials” In Brown L. et al. management in retailing: A Brit- (Eds.) State of the World, pp. 39- ish perspective”, Journal of Busi- 55. New York: Norton. ness Ethics, Vol. 23, No. 1, pp. 19

- 23. International Journals Call for Paper The IISTE, a U.S. publisher, is currently hosting the academic journals listed below. The peer review process of the following journals usually takes LESS THAN 14 business days and IISTE usually publishes a qualified article within 30 days. Authors should send their full paper to the following email address. More information can be found in the IISTE website : www.iiste.org Business, Economics, Finance and Management PAPER SUBMISSION EMAIL European Journal of Business and Management EJBM@iiste.org Research Journal of Finance and Accounting RJFA@iiste.org Journal of Economics and Sustainable Development JESD@iiste.org Information and Knowledge Management IKM@iiste.org Developing Country Studies DCS@iiste.org Industrial Engineering Letters IEL@iiste.org Physical Sciences, Mathematics and Chemistry PAPER SUBMISSION EMAIL Journal of Natural Sciences Research JNSR@iiste.org Chemistry and Materials Research CMR@iiste.org Mathematical Theory and Modeling MTM@iiste.org Advances in Physics Theories and Applications APTA@iiste.org Chemical and Process Engineering Research CPER@iiste.org Engineering, Technology and Systems PAPER SUBMISSION EMAIL Computer Engineering and Intelligent Systems CEIS@iiste.org Innovative Systems Design and Engineering ISDE@iiste.org Journal of Energy Technologies and Policy JETP@iiste.org Information and Knowledge Management IKM@iiste.org Control Theory and Informatics CTI@iiste.org Journal of Information Engineering and Applications JIEA@iiste.org Industrial Engineering Letters IEL@iiste.org Network and Complex Systems NCS@iiste.org Environment, Civil, Materials Sciences PAPER SUBMISSION EMAIL Journal of Environment and Earth Science JEES@iiste.org Civil and Environmental Research CER@iiste.org Journal of Natural Sciences Research JNSR@iiste.org Civil and Environmental Research CER@iiste.org Life Science, Food and Medical Sciences PAPER SUBMISSION EMAIL Journal of Natural Sciences Research JNSR@iiste.org Journal of Biology, Agriculture and Healthcare JBAH@iiste.org Food Science and Quality Management FSQM@iiste.org Chemistry and Materials Research CMR@iiste.org Education, and other Social Sciences PAPER SUBMISSION EMAIL Journal of Education and Practice JEP@iiste.org Journal of Law, Policy and Globalization JLPG@iiste.org Global knowledge sharing: New Media and Mass Communication NMMC@iiste.org EBSCO, Index Copernicus, Ulrich's Journal of Energy Technologies and Policy JETP@iiste.org Periodicals Directory, JournalTOCS, PKP Historical Research Letter HRL@iiste.org Open Archives Harvester, Bielefeld Academic Search Engine, Elektronische Public Policy and Administration Research PPAR@iiste.org Zeitschriftenbibliothek EZB, Open J-Gate, International Affairs and Global Strategy IAGS@iiste.org OCLC WorldCat, Universe Digtial Library , Research on Humanities and Social Sciences RHSS@iiste.org NewJour, Google Scholar. Developing Country Studies DCS@iiste.org IISTE is member of CrossRef. All journals Arts and Design Studies ADS@iiste.org have high IC Impact Factor Values (ICV).