El documento describe un programa de auditoría especial para evaluar la administración del almacén central entre enero de 2015 y marzo de 2016. El objetivo es emitir una opinión independiente sobre la auditabilidad del almacén y obtener información suficiente para llevar a cabo la auditoría. El programa incluye 11 procedimientos como solicitar documentación, verificar registros de inventario, realizar un inventario sorpresivo y elaborar un informe final.

SLTS kernel and base-layer development in the Civil Infrastructure PlatformYoshitake Kobayashi

The Civil Infrastructure Platform (CIP) is creating a super long-term supported (SLTS) open source "base layer" for industrial grade software. We have been working on security fixes and some backported features since the moment we decided that Linux kernel v4.4 would be the first SLTS version. In this talk, we will describe the current development status of the SLTS kernel and testing environment. First, we'll explain our kernel development policy. Then, we'll describe the functionality that has been backported. Second, we'll talk about testing before using our base-layer on real products. We have been developing a test framework to collect and share test results. To build it, we don't want to duplicate existing work such as KernelCI, Fuego and others. For that reason, we are trying to collaborate and contribute to such projects. And finally, we'll discuss the future roadmap.

الاثار الاقتصادية للغزو العثماني - دراسة حالة لإستنزاف الفائض في مصر العثمانيةالدكتور محمد مدحت مصطفى

قرية الأنبوطين وتوابعها بمصر السفلي 1798م.

*تقع قرية الأنبوطين وتوابعها بقلولة ومنية حبيش بولاية الغربية. وقد بلغ زمام تلك القرية وتوابعها 3209 فدان من بينها 56 فدان أراضى رزقة بأسماء أشخاص ومعفاة من الضرائب، و31 فدان أراضى بور ومنافع، ثم أرض الالتزام وبلغت مساحتها 3122 فدان من بينها 171 فدان أرض أوسية و2651 فدان أراضى فلاحة.

*أضيف إلى ضريبة الميرى التي تم تحصيلها ضريبة أخرى باسم المضاف، وبالتالي يصبح إجمالي المال الحر 361558 باره خصمت منها مصاريف محلية قدرها 63508 باره ليصبح صافى المال الحر 298050 باره يتم توزيعه بين السلطان وحاكم الولاية فيما عرف باسم الكشوفية القديمة (مال الجهات، وخدمة العسكر، وكلفة السلطان) والملتزم.

*ثم دفعت تلك القرية ضرائب أخرى تحت تسميات ثلاث: براني قديم، وبراني جديد، كشوفية جديدة. وبعد إضافة هذه الضرائب الثلاث إلى صافى المال الحر السابق تقديره يصبح الإجمالي العام 622536 باره.

SLTS kernel and base-layer development in the Civil Infrastructure PlatformYoshitake Kobayashi

The Civil Infrastructure Platform (CIP) is creating a super long-term supported (SLTS) open source "base layer" for industrial grade software. We have been working on security fixes and some backported features since the moment we decided that Linux kernel v4.4 would be the first SLTS version. In this talk, we will describe the current development status of the SLTS kernel and testing environment. First, we'll explain our kernel development policy. Then, we'll describe the functionality that has been backported. Second, we'll talk about testing before using our base-layer on real products. We have been developing a test framework to collect and share test results. To build it, we don't want to duplicate existing work such as KernelCI, Fuego and others. For that reason, we are trying to collaborate and contribute to such projects. And finally, we'll discuss the future roadmap.

الاثار الاقتصادية للغزو العثماني - دراسة حالة لإستنزاف الفائض في مصر العثمانيةالدكتور محمد مدحت مصطفى

قرية الأنبوطين وتوابعها بمصر السفلي 1798م.

*تقع قرية الأنبوطين وتوابعها بقلولة ومنية حبيش بولاية الغربية. وقد بلغ زمام تلك القرية وتوابعها 3209 فدان من بينها 56 فدان أراضى رزقة بأسماء أشخاص ومعفاة من الضرائب، و31 فدان أراضى بور ومنافع، ثم أرض الالتزام وبلغت مساحتها 3122 فدان من بينها 171 فدان أرض أوسية و2651 فدان أراضى فلاحة.

*أضيف إلى ضريبة الميرى التي تم تحصيلها ضريبة أخرى باسم المضاف، وبالتالي يصبح إجمالي المال الحر 361558 باره خصمت منها مصاريف محلية قدرها 63508 باره ليصبح صافى المال الحر 298050 باره يتم توزيعه بين السلطان وحاكم الولاية فيما عرف باسم الكشوفية القديمة (مال الجهات، وخدمة العسكر، وكلفة السلطان) والملتزم.

*ثم دفعت تلك القرية ضرائب أخرى تحت تسميات ثلاث: براني قديم، وبراني جديد، كشوفية جديدة. وبعد إضافة هذه الضرائب الثلاث إلى صافى المال الحر السابق تقديره يصبح الإجمالي العام 622536 باره.

GESTIÓN DE ALMACENAMIENTO : Almacenar hoy es una desventaja es mucho mejor mantener un inventario holgado que permita le flujo de caja, debemos utilizar herramientas para mejorar la rotación de los productos y tener una duración controlada.

EL MERCADO LABORAL EN EL SEMESTRE EUROPEO. COMPARATIVA.ManfredNolte

Hoy repasaremos a uña de caballo otro reciente documento de la Comisión (SWD-2024) que lleva por título ‘Análisis de países sobre la convergencia social en línea con las características del Marco de Convergencia Social (SCF)’.

“La teoría de la producción sostiene que en un proceso productivo que se caracteriza por tener factores fijos (corto plazo), al aumentar el uso del factor variable, a partir de cierta tasa de producción

normas de informacion financiera nif b-8 y nif b-7

11111111111111

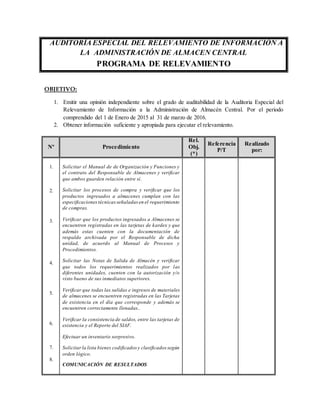

1. AUDITORÍA ESPECIAL DEL RELEVAMIENTO DE INFORMACIÓN A

LA ADMINISTRACIÓN DE ALMACEN CENTRAL

PROGRAMA DE RELEVAMIENTO

OBJETIVO:

1. Emitir una opinión independiente sobre el grado de auditabilidad de la Auditoria Especial del

Relevamiento de Información a la Administración de Almacén Central. Por el periodo

comprendido del 1 de Enero de 2015 al 31 de marzo de 2016.

2. Obtener información suficiente y apropiada para ejecutar el relevamiento.

Nº Procedimiento

Rel.

Obj.

(*)

Referencia

P/T

Realizado

por:

1.

2.

3.

4.

5.

6.

7.

8.

Solicitar el Manual de de Organización y Funciones y

el contrato del Responsable de Almacenes y verificar

que ambos guarden relación entre sí.

Solicitar los procesos de compra y verificar que los

productos ingresados a almacenes cumplan con las

especificacionestécnicasseñaladas en el requerimiento

de compras.

Verificar que los productos ingresados a Almacenes se

encuentren registradas en las tarjetas de kardex y que

además estas cuenten con la documentación de

respaldo archivada por el Responsable de dicha

unidad, de acuerdo al Manual de Procesos y

Procedimientos.

Solicitar las Notas de Salida de Almacén y verificar

que todos los requerimientos realizados por las

diferentes unidades, cuenten con la autorización y/o

visto bueno de sus inmediatos superiores.

Verificar que todas las salidas e ingresos de materiales

de almacenes se encuentren registradas en las Tarjetas

de existencia en el día que corresponde y además se

encuentren correctamente llenadas..

Verificar la consistencia de saldos, entre las tarjetas de

existencia y el Reporte del SIAF.

Efectuar un inventario sorpresivo.

Solicitarla lista bienes codificados y clasificados según

orden lógico.

COMUNICACIÓN DE RESULTADOS

2. 9.

10.

11.

Prepare planillas de deficiencias identificado los

atributos de Condición, Criterio, Causa, Efecto y

Recomendación y realice la referencia y correferencia.

En base a los resultados obtenidos, elabore el Informe

de Relevamiento determinando la auditabilidad o no

del Área de Almacenes..

Referencie y correferencia los papeles de trabajo así

como la documentación de respaldo.

Elaborado por:

Auditor Interno

Revisado por:

Supervisor

Aprobado por:

Jefe Auditoria Interna